There’s an old adage, “If something sounds too good to be true, it probably is”. The real estate deal you’re about to read about happens to fit that saying perfectly. Everything seemed great going in, but not everyone made it out alive. Read on to find out who bit the bullet, and who walked away unscathed.

A few weeks after I personally met Matt Faircloth, he called me about an opportunity in the Point Breeze section of South Philadelphia. If you haven’t read about my initial in-person meeting with Matt, you can do so here. It was the day I learned about Private Money Lending as an investment strategy. Up until that point, I was under the impression that I’d be a turn-key investor. Thankfully, that didn’t happen. Anyway, Matt calls me one morning and says he has a row house in South Philly under contract for $115K. “The property is in a gentrifying neighborhood. There are cranes on every other block, redevelopment is booming.” He ended his pitch by telling me he just flipped and sold a house that went for full ask within the first 24 hours of being listed just a few blocks away. Needless to say, I was excited. I asked him to send me the information via email. I like to look at the data. Read it, study it, digest it, and take notes as I go along. Here’s what I requested:

- Address

- Detailed Acquisition Cost + Rehab Budget

- Comp Sales

- Comp Rents

- Promissory Note

- Mortgage Terms

Before hanging up the phone, Matt sprung a final surprise on me: scarcity. “By the way, the closing is on Friday, so we need to know if you can do this by tomorrow latest. If you can’t, I’ll have to call other investors.” He pounded my millennial FOMO button with a sledgehammer.

The information for the deal came in an email within the hour. I was basically sitting at my computer clicking the refresh button waiting for it.

The sales comps checked out. I would love to provide a screenshot, but the link he forwarded me from the MLS expired (Sorry!!). We were looking at being all in (Acquisition, Rehab, and Holding Costs) for $225K. The sales comps were all at or above $295K. A good $70K buffer.

To be safe, I asked Matt to check the rental comps. This was an over-cautious step. In no scenario were either of us going to hold onto this property as a rental. In retrospect, I was just looking for another validating data point. Regardless, the rental comps were healthy. In the absolute worst case scenario, I would refinance all the money ($225K) out with a traditional mortgage and cover the PITI (Principal, Interest, Tax, & Interest) easily on a $295K appraisal with 75% LTV (Loan To Value).

- $295K * 75% = $225K. The 30 year loan would cover my money in the deal.

- $225K at 5% interest amortized over 30 years = 1,200 per month (Principal & Interest).

- Taxes on this property were 100 per month.

- Insurance would be another 100 per month.

- Maintenance and CapEx would be 100 per month. (Super conservative estimate since this property would be basically brand new).

So that puts my monthly outflow at ($1,200 + $100 + $100 + $100) $1,500. Comparable rents were in the $1,700 – $1,800 range for a 2 bed 1.5 bath unit in the area. I wasn’t thrilled about $200 per month in potential cash flow, but knowing that’s one of the “worst case” scenarios was fine with me.

?Deep Dive Into The Numbers:

|

Closing Costs & Expenses |

Finance Purchase |

|

Est. Purchase Price |

$110,000.00 |

|

Est. Rehab |

$95,000.00 |

|

Loan amount |

$205,000.00 |

|

Carrying costs |

$7,725.00 |

|

Loan Origination Fee |

$0.00 |

|

Down Payment |

$0.00 |

|

Appraisal |

$0.00 |

|

Title Charges |

$1,870.00 |

|

Transfer Tax 2% |

$2,200.00 |

|

Government Recording |

$726.00 |

|

Construction management fee (4 MONTHS AVERAGE) |

$4,000.00 |

|

TOTAL INVESTOR CAPITAL |

$221,521.00 |

|

AVERAGE SALES PRICE |

$300,000.00 |

|

2017 REAL ESTATE TAX |

$1,021.00 |

|

REMAX FEE |

$345.00 |

|

Other |

$0.00 |

|

Title Charges |

$96.00 |

|

Transfer Tax 2% |

$6,000.00 |

|

Commission (Buyer 2.5%) |

$7,500.00 |

|

Commission (Seller 2%) |

$6,000.00 |

|

CLOSING COSTS SELLING |

$20,962.00 |

|

|

|

|

Carrying Costs |

|

|

Utilities |

$600.00 |

|

Insurance |

$900.00 |

|

Staging |

$0.00 |

|

Appliances |

$3,650.00 |

|

Architect |

$2,500.00 |

|

New PECO service |

$75.00 |

|

Total |

$7,725.00 |

|

FINAL COSTS |

|

|

Items |

|

|

TOTAL INVESTOR CAPITAL |

$221,521.00 |

|

Closing costs selling |

$20,962.00 |

|

Total |

$242,483.00 |

|

After Repair Value |

$300,000.00 |

|

PROFIT |

$57,517.00 |

|

INVESTOR PREFERRED RETURN |

$8,860.84 |

|

10% |

$4,865.62 |

|

90% |

$43,790.54 |

|

50/50 |

$21,895.27 |

|

Total Investor Return |

$13,726.46 |

|

ROI in 6 Months |

6.20% |

|

Actual annualized return |

12.39% |

?Lessons Behind The Numbers:

Before we go any further, I want to address the lessons learned so far:

- I arranged financing for 100% of the deal: 100% of acquisition + 100% of rehab.

- I would never do this again, but I didn’t know any better.

- Thankfully, it didn’t come back to bite me in the butt.

- I didn’t charge any points or origination fees. (These are typically 1-3% of the total loan amount).

- I should have. Everyone else does.

- I paid 4% interest to borrow the money. I turned it around at 8%. Not a great arbitrage.

- I sacrificed 4% in interest to be a 10% partner on the profit.

- Meaning, I could have received 12% instead of 8%.

- This turned out to be a mistake.

- Never doing this again. You’ll find out why as you read on.

- I sacrificed 4% in interest to be a 10% partner on the profit.

Matt wanted me to wire over the acquisition + the entire rehab budget (~225K) at close. I wasn’t willing to do this. I’ve been in hot water by prepaying general contractors before. Also, this was my first deal with Matt. And I was financing 100% of it. We had to come to another agreement.

I asked him to trust that I was going to hold the money in “escrow” for him. We added a last minute caveat to the deal where the non-distributed rehab funds held in escrow would make 4% instead of the full 8% while not in use (This helped me cover the cost of my money).

??♂️Construction Draw Schedule:

- General Contractor Deposit: $20K for Permits, Demo, Digging Basement, Concrete Slab, Framing & Windows

- $20K: Roof, Stucco, Concrete Backyard, Fence, Rough Mechanical (Electrical, Plumbing, HVAC)

- $20K: Insulation, Drywall, Doors, Trim

- $25K: Flooring, Kitchen, Final Mechanical (Electrical, Plumbing, HVAC), & Finishes

- $10K: Final Punchlist + Certificate of Occupancy

?The Transformation:

The property was acquired on 4/12/2017.

I went down to see the property on 4/18/2017.

By the time I got there, renovation was well underway. Here are some pictures from demo and phase 1 (framing & windows):

This basement floor is brand new. In order to add the basement as usable square footage in the listing, the team had to dig the floor down to meet the city’s height clearance requirement of 9 feet.

So as you can see, the renovation team had their work cut out for them.

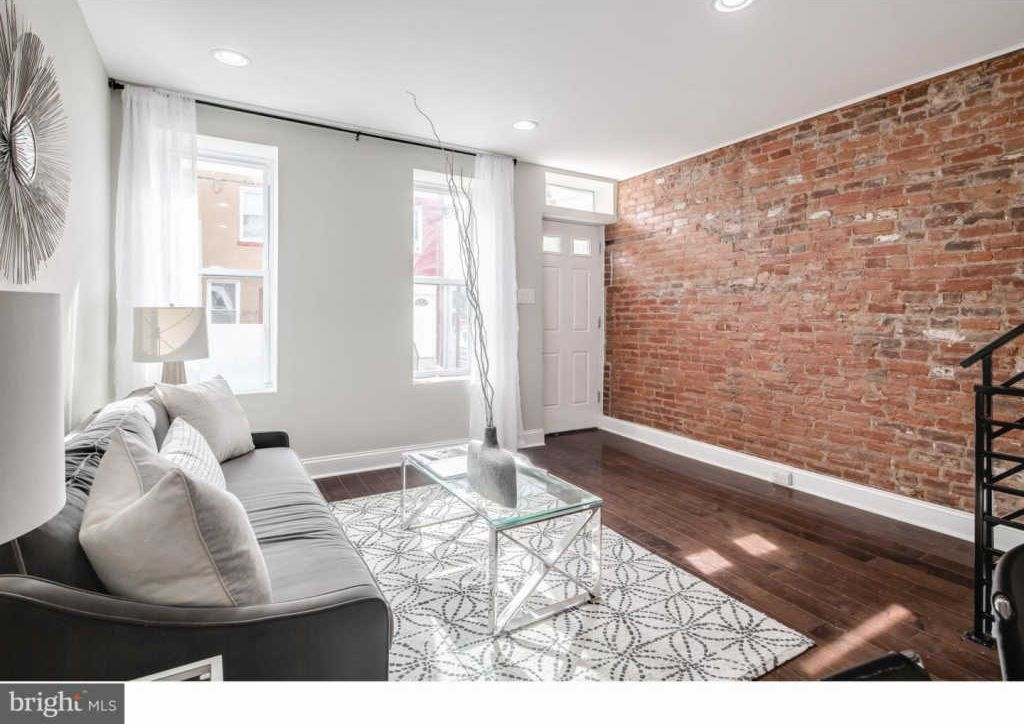

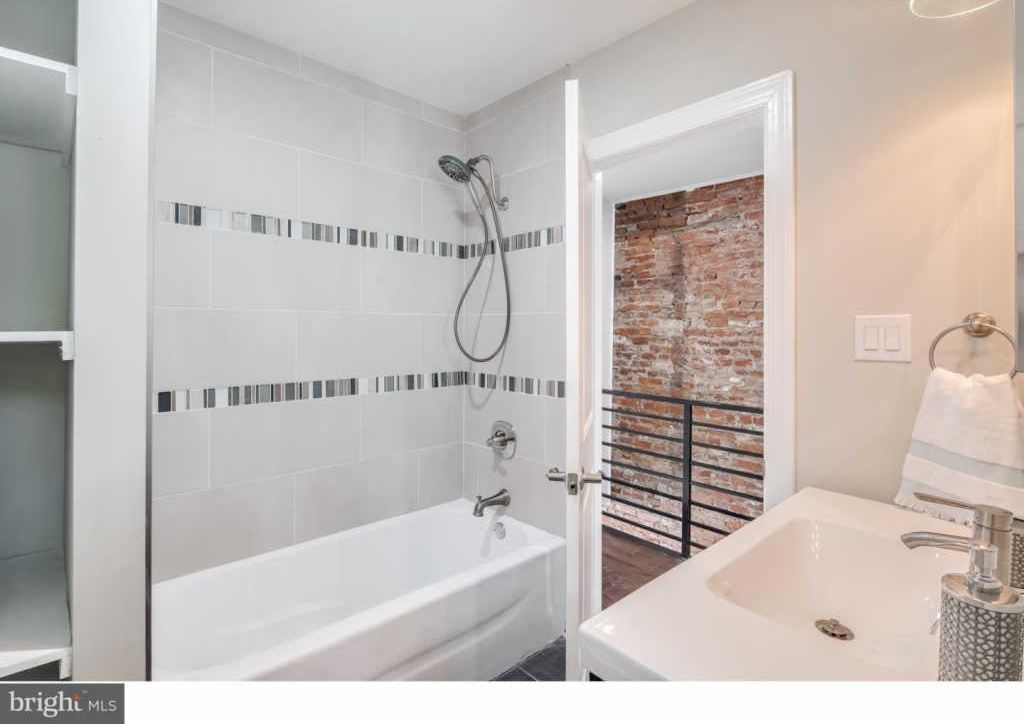

The final product came out EXCELLENT.

Here are some photos from the listing:

What a difference! My absolute favorite part of the house is the exposed brick along the staircase. It adds so much character. My last visit to this property was about 2 weeks before it was listed, so I never saw the final product in person, but I imagine it looked great and showed well.

?Too Much Competition:

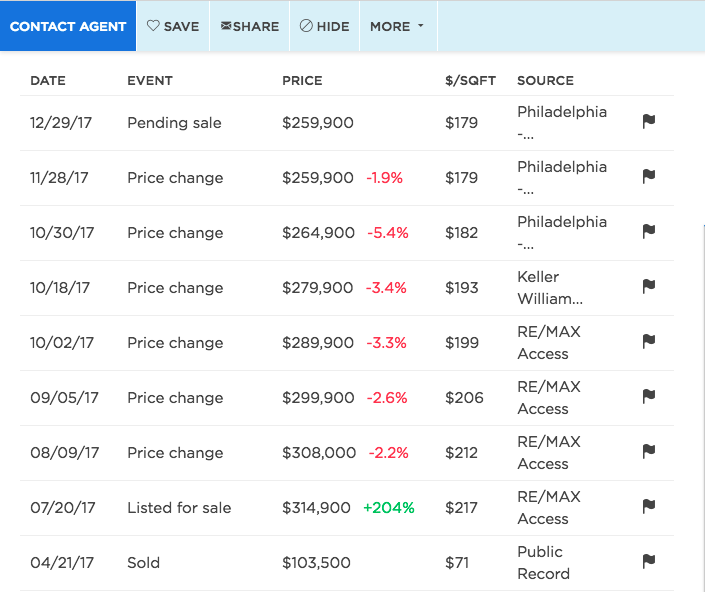

Matt’s team listed the home on July 20th, 2017. The final sale closed on January 31st, 2018. Whoa!5+ months on the market! What happened to the first deal in this area with offers coming in at full ask within 24 hours?

Each time I went down to visit this property, it seemed like another property was undergoing renovation. At the time, the area’s redevelopment seemed like a good sign, but it wasn’t. When you looked at the MLS, or Zillow for that matter, almost every property for sale was completely renovated product. So pricing became a race to the bottom. Not to mention, our floor plan was small. We only had 2 beds and 1.5 baths. Not ideal.

It took 6 price drops to finally get this property under contract. The image below shows how that shook out in detail. Start at the bottom and work your way up.

After final negotiations, the house sold for $250,000. You must be wondering if any money was made on this deal.

Here’s where we come back to why I’ll never sacrifice interest percentage points for Joint Venture upside. On this particular deal, there was no profit. In fact, the property sold at a loss. The 8% Interest I charged on my money turned out to be around $15K. So $225K + $15K = $240K. Then there was about $15K in additional soft costs that made my partner lose around $5K on this deal.

Thankfully, my Joint Venture (10%) portion was structured as a fee, instead of actual equity. If it was equity, I would have had to eat 10% of the loss. Which in this case would have been $500. At the same time, if I had stuck to 12% interest and no Joint Venture Equity, the interest I charged on my money would have been closer to $22,500.

Even if the property sold at our projected $295K, the profit would have been ~$40K. I would have taken $4K of that. So my total return would have been $15 + $4 = $19K. Still less than if I had just charged 12% from the beginning.

While I’m not ecstatic about the outcome, I am grateful that we didn’t lose money on the deal. That’s the importance of being in the first lien position. When the home sells, you get paid what you’re owed first. Then profits (or losses) get distributed.

❗Final Takeaways:

A bird in hand is worth two in the bush. At first, Matt offered me 12% simple interest. I balked at that offer in exchange for 8% simple interest + 10% Joint Venture Fee on Profits. This ended up being a $7.5K mistake. Won’t do this again.

Make sure the GC / Developer has skin in the game. I was proud of myself for holding back construction funds in escrow. I’d be more proud if I didn’t lend 100% of acquisition cost. Going forward, I’m going to make sure I fund no more than 80% of Acquisition while still holding the first lien on the property.

Do business with good people. This flip was “upside down”. Which means it sold for less than we had in it. Matt never once asked for a break of any sort. He had to bring a check to close so I could be made whole.

Reputation matters. The buyer of the house mentioned she chose this property over another because she read, listened to, and watched a bunch of Matt’s content on the internet.

Before You Leave:

I’d love to hear your take! Let me know how I did. Please leave a comment below with your thoughts or any questions you might have. Also, make sure to sign up for my newsletter. That will ensure you don’t miss my next post!

SUBSCRIBE NOW TOSUNSHAKSUNDAY

Join my newsletter if you want to learn more about real estate investing, personal finance, health & fitness, and so much more.