My parents came to the US in the early 80s, a couple years before I was born. If you’re a first generation American in an Asian family, we’re practically siblings. We grew up with a basic understanding of a few things. 1) Always finish the food on your plate. 2) Don’t wear shoes in the house. 3) Education over everything. Finally, never (EVER) waste money on rent!

Today, you’ll read about that last tenet: the belief that renting is a waste of money. Maybe I’m writing this to assuage my own guilt. After all, our rent is pricey for a 2 bedroom + 2 bathroom in Parsippany, NJ. We live in one of those buildings with all the bells and whistles. There’s a dog-washing station and dog park. There’s an electric vehicle charging station in the garage. There’s a coffee station we hit every morning before work. Finally, my favorite amenity: the courtyard with a pool, fire pit, and barbecue grills.

It’s July 2018 and we moved into this amenity filled building in April of 2018. For context, I thought the idea of renting was crazy up until July of 2017. There’s only one story I need to tell you to display how opposed to the idea of renting I used to be.

Dia and I did our court marriage back in January 2014. Our wedding wasn’t until October of 2015 (because of early financial struggles). We stayed in the bedroom next to my parent’s room until July 2016!!! Facepalm, for reals.

Although we finally moved out of my parents house in July 2016, I did so reluctantly. I spent MONTHS trying to delay the move. We visited countless apartment complexes. I’d always complain about the commute distance, traffic, weird smells, etc. I’d find any reason to not rent. I wanted to move out of my parents place, but I didn’t want to rent!

My invisible script of renting being a poor financial decision lead me to subconsciously sabotage my wife’s efforts. All she was trying to do was kick-start our life together as a married couple.

When I finally realized that we wouldn’t have a down payment for a home in “just another couple months” I gave in. Well, I kind of gave in. I joined the search party to find a suitable apartment. Cost was obviously my number one priority. I wanted to get the most “valuable” apartment we could find.

We landed on a garden style building in Wayne, NJ for $1,450 per month. This was not the least expensive place we saw, but it was far from the most expensive. It was in a safe neighborhood between both our jobs and our landlord ended up being an awesome person to rent from. (Thanks Kathy!)

Our original plan was to stay in that apartment for one year. Save up enough cash for a down payment on a starter condo / town- home and never rent again.

But then two things happened…

One. Some of my friends who were buying homes around that same time started complaining. The time and effort they spent maintaining their homes became cumbersome. It seemed like every weekend, people had to clear their gutters, take care of their landscaping, buy a new set of appliances, fix a leak in their oil tank, get a quote for a new roof, etc, etc.

Two. I started to consume content about the pros and cons of renting vs. buying. Here are a few of my favorite articles that discuss the topic in depth:

- Renting is Throwing Money Away Right?

- Why Your House Is A Lousy Investment by JL Collins – Courtesy of Ben in the Comments Section.

- Real Estate Investing: the Myths, Facts, & Ways to Get Started

- Pay special attention to the argument made in Myth #2: You’re Throwing Money Away if You Keep Renting.

So the new knowledge I acquired and the constant demands on my friends’ time as homeowners had me second guessing a long held belief. Is renting really all that bad?

To begin answering that question, let’s walk through two math problems!

Let’s start with the following basic assumptions:

-

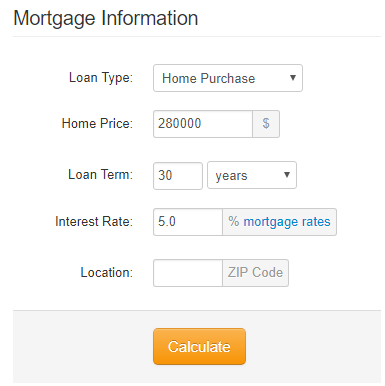

We’ll use a $350,000 home

-

Typically you would typically put 20% down ($70,000).

-

Your total loan amount would be 80% ($280,000)

-

Let’s say your interest rate is 5% fixed over 30 years.

-

Your loan starts in January 2019.

-

Your monthly payment would be $1,503.

You can follow along by entering my assumptions here.

**After clicking Calculate, change the Start Date to Jan 2019.**

Exercise 1 – Principal Portion Exceeds Interest Portion of Payment

If your loan starts in January 2019, it would take until February 2035 for the principal portion of your payment to exceed the interest portion. At the end of February 2035, you’re principal balance remaining on the loan would be $179,845. In that time, you acquire $100,155 of equity in your home. *Reference chart below

Now let’s take this exercise one step further.

-

February 2035 – January 2019 = 16 years and 1 month.

-

16 years * 12 months / year + 1 month = 193 months.

-

193 months * $1,503 / month = $290,079 in total payments.

-

$290,079 (total payments) – $100,155 (equity acquired) = $189,924 paid in interest.

$189,924 in interest paid over 16 years and 1 month is almost DOUBLE the $100,155 equity acquired.

Exercise 2 – What % of Total Payments is Interest in First 10 Years of Mortgage?

Now, let’s look at the math for the first 10 years of the loan.

-

December 2028 (exactly 120 payments) the principal balance is $227,758.

-

$280,000 (original loan amount) – $227,758 (balance) = $52,242 equity acquired.

-

$1,503 / month * 120 months = $180,360 total payments made.

-

$180,360 (total payments made) – $52,242 (equity acquired) = $128,118 total interest paid.

-

$128,118 / $180,360 = 71% of your payments for the first 10 years were interest only.

?What’s The Alternative?

When someone asks the question, “Should I rent or buy?”, the answer is always, “It depends!”. Unfortunately, there is no one size fits all remedy. However, I’m going to continue to outline my specific scenario based on where we live and what our alternatives are. Our scenario may not be the same as yours, so you have to adjust accordingly.

The first thing I did was find a comparable home that I would buy. Lucky for me, one of my cousins lives in a place that I would love to call home. It’s a beautiful townhouse that has 3 bedrooms, 3.5 bathrooms, and a flex space that can be converted into an extra bedroom, if necessary.

A quick conversation through text message revealed the numbers I needed to know.

-

Current Price: $450,000

-

Annual Property Tax: $8,000

-

Annual Insurance: $1,200

-

Annual HOA Fees: (Homeowners Association): $3,600

-

Annual Maintenance: $1,200

We can then start to make the following assumptions:

-

20% Down Payment: $90,000

-

80% Loan: $360,000 @ 5% over 30 years

-

Monthly Principal & Interest Payment: $1,933

-

5% Closing Costs: $22,500

The 13 year figure is the average length of time a family spends in one home. That honestly sounds like a long time to me, but let’s go with it.

-

13 Years of Payments: $1,933 * 12 months * 13 years = $301,548

-

Principal Balance Remaining on Loan @ End of Year 13: $265,223

-

Principal Gained on Loan @ End of Year 13: $360,000 – $265,223 = $94,777.

-

Interest Paid @ End of Year 13: $301,548 – $94,777 = $206,771

So in this 13 years of monthly payments, the only thing we get to keep is our $94,777 of principle gained. Everything else is basically a cost. Money spent that we won’t ever see again. Similar to rent.

So let’s add all those monthly COSTS together in this 13 year home ownership example.

-

Interest: $206,771 / 13 / 12 = $1,325 / month

-

Property Taxes: $8000 / 12 = $666.66 / month* assuming no growth

-

Insurance: $1,200 / 12 = $100 / month* assuming no growth

-

HOA Fees: $3,600 / 12 = $300 / month* assuming no growth

-

Maintenance: $1,200 / 12 = $100 / month* assuming no growth

-

Closing Costs: $22,500 / 13 / 12 = $145 / month

Total NON-RECOVERABLE home ownership expenses: $2,636.66 / month for 13 years.

At this point, I’m starting to make sense, but you’re still unsure. I can see the gears turning in your head. Or better yet, maybe they’ve stopped turning. They’re slowing down. Because everything you thought about home ownership being better than renting is slowly being grinded away.

?Taxes & Interest:

One benefit of home ownership is the ability to write off property taxes and interest. In 2018, a new tax plan was passed under President Trump, which doubled the standard deduction. However, to counterbalance the increase in standard deduction, changes were made to a homeowner’s ability to write off taxes and mortgage interest.

Taxes: The new law limits our ability to write off state income and local property tax to the tune of $10,000. This is down from no limit previously. To take full advantage of this $10,000, we only have a few options. We can 1) Make less money. 2) Downsize. or, 3) Move to cheaper states (namely non-coastal markets like NY/NJ/CA).

Interest: The new law limits our ability to write off interest on mortgages less than $750,000, down from $1MM previously. Safe to say not a lot of people will be affected by this change.

So what can we add back in? Let’s look at the 2018 Tax Brackets (Pulled from NerdWallet):

Dia and I fall into the 22% tax bracket today. Let’s be generous and say we’ll be 24% in the next few years. Let’s also assume we would be able to write off the full $10,000 for state income and local property tax. Then we’ll take the interest from the “What’s The Alternative?” home example immediately above.

- $10,000 * 24% = $2,400 in State Income & Local Property Tax Back Per Year

- $206,771 / 13 years = $15,905 average interest paid / year.

- $15,905 * 24% = $3,817 in Interest Tax Back Per Year.

- $2,400 + $3,817 = $6,217 Total Tax Back Per Year From Taxes & Interest

- $6,217 / 12 = $518 / month.

So if we take our $2,636.66 of NON-RECOVERABLE costs per month from above, and add the benefit of reducing our tax burden by $518 per month over the next 13 years, we are now at $2,118.66 in NON-RECOVERABLE costs per month ($2,636.66 – $518 = $2,118.66).

❓What About Appreciation?

There is one more argument I want to make before I get into the intangible stuff: you can’t count on appreciation. So don’t. Housing prices do tend to go up, but so does another little thing called inflation.

Meaning, yes, you could have bought a home for $50K in 1982, and see that it’s valued at $175K in 2017. But when you adjust for inflation, the purchase price of that home in 1982 was actually $125K. Ouch. $50K growth of purchasing power in 35 years? That’s not good!

The other downside to appreciation or home prices is you can’t time the market. Can you imagine if you bought a home in 2006 and held onto it for the average time of 13 years until 2019. You’d be lucky to break even. Most people in this scenario walked away from their homes and had them foreclosed on.

Most people are not real estate investors that know how to force appreciation in a property. For that reason alone, I will not be including the false positive benefits of appreciation into my calculations.

??Intangible Benefits of Renting

For the people that make decisions with the right brain, like my lovely wife, Dia, please continue reading. I’m now going to explain the benefits of renting from a subjective standpoint.

You can rent nicer than you buy

Most people don’t buy homes with amenities like a pool, gym, lounge, coffee bar, etc. However, these amenities are common in many apartment communities.

You can rent the perfect size and minimize your footprint

If someone pointed a gun to our head and forced us to buy today, we’d likely buy more than we need. We’d probably buy a home with 4-5 bedrooms and 3-4 bathrooms spanning at least 2,400 square feet. Why would we buy a home so big when it’s still just the two of us? Because we expect our family to grow over the next couple years and we probably couldn’t afford bigger and bigger 20% down payments every time we need to upsize.

Instead, we rent what we need for our current situation. Renting gives us the ability to meet our requirements of today. Which is 2 bedrooms and 2 bathrooms. We don’t have an abundance of extra space to clean, heat, cool, etc.

Renting keeps you flexible (and mobile)

If you buy, you’re stuck. Houses are illiquid assets. They are super hard to get in and out of. So if you end up not loving the area, or your neighbors suck, or you get a new job in a different location, picking up and moving isn’t so easy. But if any of those things happen while you’re renting, you can get out at the end of your lease. If things get dire, you can probably pay a “break-lease-fee” and walk away free and clear. Paying that break-lease-fee is definitely less expensive than the seller’s closing costs on a home.

Maintenance & Hassle Free

This has to be my favorite part of renting. If Dia clogs the shower with her hair, or I clog the toilet with my….you know… a few taps on my phone will have it fixed by the time we get home tonight. We don’t have to worry about cutting grass, shoveling snow, cleaning gutters, or raking leaves.

The only maintenance thing I’ve done over the past two years was change a light bulb. However, in that same time, we’ve had more than a handful of maintenance items taken care of for us for free.

Wrapping Up

I’ll be perfectly honest. Even though I’ve spent considerable time running the numbers, and my brain accepts that renting is actually advantageous for our specific situation. My heart still hurts a little every time the rent check goes out.

I wrote this article from a stance of defending renters. However, I will admit there are a few benefits of home ownership as well. Personally, the biggest advantage I see in home ownership is forced savings. If you’re not good at saving money, home ownership is probably better for you, even if it’s more expensive than renting.

Typically speaking, renting your home makes more sense in higher cost of living areas (New York City, Los Angeles). A good “back-of-the-napkin” way to help decide if you should rent or buy is by dividing your monthly rent by the purchase price of your home. If that number is 1% or lower, you should probably rent. If that number is 1% or higher, you should probably buy. If it’s .75% – 1.25% you should probably take a hard look at the numbers and decide what’s best for you and your family.

When you look at your numbers, be sure to look at the bigger picture. If you rent close to work, but need to buy far away, you will likely add to your transportation expense. If you rent a 1br with your new spouse, but want to buy, how big will it need to be to satisfy your needs for the next 13 years?

At this point in our lives, Dia and I will continue to rent where we live, and invest where it makes sense.

What are you going to do? Let me know in the comments below.

RESOURCES:

If you want to learn more about this topic please visit the Renting Vs. Buying A Home Course by Khan Academy.

If you want to know how much you can spend on rent by plugging in the actual numbers from your Alternative, you can do so by downloading this spreadsheet, also created by Khan Academy. Only change the fields highlighted in yellow. https://www.khanacademy.org/downloads/buyrent.xls

Before You Leave:

I’d love to hear your take! Let me know how I did. Please leave a comment below with your thoughts or any questions you might have. Also, make sure to sign up for my newsletter. That will ensure you don’t miss my next post!

SUBSCRIBE NOW TOSUNSHAKSUNDAY

Join my newsletter if you want to learn more about real estate investing, personal finance, health & fitness, and so much more.