When people who are parents find out Dia and I are pregnant with our first child, the response is always the same. “You’re going to struggle with X, but it’s all worth it.”

- You’re going to lose a lot of sleep, but it’s all worth it.

- You’re going to completely lose your routine, but it’s all worth it.

- You’re going to get peed, pooped, and vomited on, but it’s all worth it.

I seriously can’t wait for BabyShak to arrive…

Because right now, the toughest thing for me is “You’re going to spend a ton of money…”

I’m just missing the part where “… it’s all worth it.”

NEWSFLASH: Having a kid is expensive!

This is something every adult kind of knows, but doesn’t fully understand until they’re on the brink of parenthood.

?Startup Costs of Having Children

The startup costs alone can be thousands of dollars. Here are a few items we’ve acquired or received as gifts in the past few months.

- $100 – Travel Crib

- $100 – Diaper Bag

- $150 – Bedside Sleeper

- $175 – DokATot

- $200 – Bouncer

- $375 – Baby Monitor

- $1,000 – Crib + Dresser

- $1,000 – Car Seat + Stroller System

We’re at $3,000+ and this list doesn’t include the countless incremental items priced in the $25 – $75 range. Without doing the math, I’d venture to guess our startup costs for BabyShak are $5,000.

If you’re thinking, “but you don’t need all that”, you’ll receive no argument from me.

As the youngest of 3 children and 4th youngest of 16 cousins, I grew up on hand-me-downs. I turned out just fine.

If you’re thinking, “I would never spend that much on things that will receive less than one year of use”, don’t be so quick!

On the scale of thriftiness, I land somewhere between Cheap AF and Frugal. However, saying “No” is damn near impossible when it comes to spending money on our first kid.

?Operating Expenses of Having Children

The startup costs mentioned above are just the tip of the iceberg. The ongoing operating expense of raising a child is the massive underwater glacier you can’t see.

I’m assuming everyone reading this watched Titanic…

Based on a 2015 report issued by the USDA, middle-income, married-couple parents of a child born in 2015 may expect to spend $233,610 ($284,570 if projected inflation costs are factored in*) for food, shelter, and other necessities to raise a child through age 17. This does not include the cost of a college education.

Based on the USDA’s study, we’re looking at an ongoing cost of $13-16K per year per child.

According this article on NJ.com, daycare or preschool alone can cost $1,025 to $1,485 per month where we live in Morris County, NJ.

?WWYD?

What would you do if you found out your total expenses are about to increase by $1,000 – $1,500 per month?

I imagine some combination of these following options as the most common approach:

- Cut out expenses that seem frivolous

- Gym membership

- Going out to eat when too lazy to cook

- Buying the latest clothing or tech on a whim

- Travel & Entertainment

- BOMAD – Bank of Mom & Dad

- My parents practically bribed us into having a kid (their first grandchild)

- Dia’s parents basically bought us the balance of our registry

- Sacrifice Savings

- Reduce contributions to retirement accounts

- Ask for a raise / promotion at work

- A $10-15K raise could help, but it won’t fill the gap because, ya know, taxes.

The biggest problem I have with this plan is it treats our current budget as a finite game.

- X = Income

- Y = Spend

- Z = Savings

The equation looks like either X – Y = Z or, if you’re in the Warren Buffet camp, you’re operating on X – Z = Y.

Here’s our given: Y (spend) is about to increase by $1.5K per month. What does that mean? Either:

- X (income) needs to go up by 1.5K to keep Z (savings) the same or

- Z (savings) needs to go down by 1.5K per month if X (income) stays the same.

The main issue I have with this finite game is the possibility of resentment in the future. The idea of “giving up” something we enjoy for the betterment of our child is obviously a no brainer. We’ll do it every time. However, I have a small fear the scar of that sacrifice could fester over time.

That’s why Dia and I plan to play an infinite game. Increase X, Y, & Z by simply increasing income.

The rest of this post explains how we plan on doing that in the immediate future. We will increase our streams of income instead of having any single income stream increase.

????Investing 4 Family

On October 18th, 2019 we signed a contract to purchase a 4-Family rental property in Collingswood, NJ. We finally closed on January 24th, 2020.

It took about 100 days to get from “I want this” to “I have this”. In that time, a lot transpired.

A wholesaler presented the property to me at a purchase price of $310,000. The original rehab budget was $90,000.

Definition:Wholesaler – someone who puts a distressed home under contract with the intent to assign that contract to another buyer.

In this case, the wholesaler put the property under agreement of sale with the seller for a purchase price of $290,000. He then tried to turn around and assign that contract to me for $310,000. He would earn the difference ($20,000) when I closed.

Before Dia and I signed the purchase and sale agreement, I was able to get the price down to $290,000. The wholesaler waived his $20,000 fee. You’ll understand how it was in his best interest to do so a little later.

This allowed me to increase the rehab budget by $20,000 to a total of $110,000.

This was the first price reduction Dia and I received on this property.

Once the purchase price was finalized, we signed the contract and sent over a refundable deposit of $5,000 to the Title company handling the transaction.

On October 30, 2019, we received a copy of the Title paperwork.

Definition:Title – the legal way of saying you own a right to something

Usually, any mortgages or liens against the property show up in the Title paperwork. This 4-family rental property didn’t have any outstanding loans or liens against it, which meant the seller owned the property free and clear. This is super uncommon, especially among investment properties. Jackpot!

Once I realized the seller owned the property free and clear, I asked the seller’s agent if the seller would consider providing seller-financing.

Definition:Seller-financing: When the seller of the property acts as the lender. Instead of going to the bank for a loan, the seller converts their equity into a loan to the new buyer.

Here was my initial offer: I wanted to put 10% down ($29,000) and the seller could charge me 5.5% interest only for 24 months on the remaining $261,000. My payment would have been $1,196.25 per month. ($261,000 x .055 / 12 = $1,196.25)

The seller countered at $40,000 down and we agreed. This was a huge step in the right direction. Seller-financing is great because you can avoid a lot of time wasted and costs associated with going through a bank.

While this was going on, I drove down to the property and to meet with the following people:

- The seller’s agent

- The seller’s property manager

- A general contractor

- Another realtor who works in that area

All 5 of us walked through all 4 units. It took about an hour. 1 unit was in good shape. The other 3 had some seriously deferred maintenance.

The contractor confirmed our rough estimate of $110,000 as feasible. “It’s mostly cosmetic”, he said. ProTip: Never take a contractor at his word. Don’t trust, just verify.

The “other” realtor gave me a good idea of what I could expect in rental income as long as we made the necessary updates.

I was feeling good, but I didn’t stop there. I hired an inspector to dig deeper.

The inspection report that followed had red tape everywhere. We needed to fully replace the electrical, plumbing, roof, and mechanicals (HVAC, hot water heater).

We sent the inspection report to the contractor so he can update his bid. He came back with $150,000! Reminder: “Mostly cosmetic.”, he said…

I was ready to walk away. But before doing so, I needed to throw an Aaron Rodgers sized hail-mary pass.

To counterbalance the $40,000 increase in rehab costs, I asked the seller’s agent to reduce the price to $250,000 and deliver the property vacant.

Delivering the property vacant ensured we could start our rehab immediately. The least expensive way to rewire the electrical system would be coming down through the roof. That way, we wouldn’t have to open up any walls.

The seller countered at $250,000 with all 4 tenants still in place.

We countered at $240,000 with all 4 tenants in place or $250,000 vacant.

He agreed to $240,000 with all 4 tenants in place.

Shit. This is happening.

I wish I could say I was proud of my negotiation skills for this transaction, but I can’t. I just asked if something was possible and got what I wanted.

Lesson learned: You miss 100% of the shots you don’t take!

1️⃣The 1% Rule

I didn’t want my acquisition and rehab to exceed $400,000. The as-is rent roll was $3,700 ($925 / unit). We were expecting the rent roll to be $4,800 per month after repairs.

There’s a rule of thumb called the 1% Rule. It’s a litmus test for whether a property is going to make for a good investment or not. The 1% rule is not enough to make a final decision on, but it is enough to warrant further analysis.

If we spent $400,000 on acquiring and improving this property, but the rents didn’t budge, we wouldn’t be ecstatic, but we also wouldn’t be shit out of luck. $3,700 / $400,000 = .925%. Close enough to 1%.

If we achieved our rent premiums and stayed within budget, we’d be way ahead. $4,800 / $400,000 = 1.2%. I’ve got a Bingo!

Keep reading and you’ll see my ProForma operating statement.

?The Kicker

After agreeing to the $50,000 price reduction, the seller pulled the seller-financing off the table. This was a major hitch in the plan. We scrambled to find a loan.

We wanted a short term interest only loan. The business plan was to rehab the property and then refinance into long term debt after adding significant value.

Reminder: The seller-financing terms were $40,000 down, 5.5% Interest Only for 24 months.

No funds for construction money, but still a good deal.

I ended up finding a lender that offered us 90% of purchase, at 7.5% Interest Only for 12 months with 100% of construction money. This means I would only have to come to closing with 10% down ($24,000) plus the cost of closing which would be about $10,000.

Total loan amount would have been $366,000. =(($240,000 * 90%) + $150,000)

These terms were on par with the seller-financing. But it was bait.

Then came the switch. The lender required an appraisal and it came back super low. We told them the value of the property would be $450,000 once finished. Our competitive market analysis supported that. The appraisal came back with an After Repair Value (ARV) of $390,000.

Why so low? There were no comparable properties. No 4-family home sold in the surrounding area in the past 3 years. However, just a few months prior, a 2-family home down the street sold for $365,000.

They said they can only lend up to $292,500 ($390,000 x 75%), we lost about 75K in leverage from their original offer.

Then the lender said we didn’t qualify for their preferred loan terms because of a lack of experience. When I submitted my resume, they said I’d easily qualify. However, since I mostly participated in deals as a minority stakeholder, they didn’t give me credit.

This increased our interest only rate from 7.5% to 8.5% per year. It also reduced our Loan to Value (LTV) ratio from 75% to 70%. So now we were looking at a total loan amount of $273,000. =($390,000 x 70%).

The last minute adjustments by the lender were hard to swallow. However, the terms were still better than I could get elsewhere.

As a last ditch effort, I asked the owner for seller-financing again. He would only do it if we increased the purchase price up to $255,000. That was a no for me, dog.

We ended up biting the bullet and closing. Dia and I will have to personally fund the remainder of the rehab budget and wait to get our money back when we refinance.

??Partnership Structure

Success is better when it is shared.

Dia and I own 100% of the LLC that owns this property.

However, we signed a side agreement with the wholesaler who brought us this opportunity.

Here are (some of) the terms of our deal:

- The wholesaler agreed to waive his $20,000 fee for bringing us the deal as well as managing the project. We assigned a cash value of $10,000 to that.

- The wholesaler agreed to manage the project. This included the entire rehab process as well as leasing the updated units at market rent. We assigned a cash value of $5,000 to that.

- Their total contribution was valued at $15,000

- Dia and I contributed $60,000 towards the acquisition and working capital for this investment. This brings the total “cash and cash equivalents” invested to $75,000.

- 60,000 / 75,000 = 80%

- 15,000 / 75,000 = 20%

- We have a 75% / 25% equity split with the wholesaler.

- We gave up 5% equity in exchange for a preferred return.

- Our preferred return is 8% on our capital account of $60,000. That means, the first $4,800 of cash flow per year comes to us. Anything above that is split 75 / 25.

- The wholesaler’s property management fee will be 4% of gross collected rent. Once we lease all 4 units at market rent, they can expect to make $200 per month in management fees. =($4,800 x .04)

- In the event of a sale or refinance, the following accounts will be paid in order:

- Costs of sale or refinance

- Outstanding Loans & Liens against the property

- Accrued Preferred Return

- Owner’s Capital Account ($60,000)

- Wholesaler’s Capital Account ($15,000)

- The rest of the proceeds will be split 75 / 25.

- Finally, there’s a 24 month termination clause. If, for whatever reason, Dia and I are not happy with their service, we can buy them out.

- First, we’d pay the $15,000 in fees they waived.

- Second, we’d pay them an additional 4% of gross collected rent since their typical management fee is 8%.

This type agreement aligns both of our interests. I’m handing over equity in exchange for project management in the short term and property management in the long term. If they don’t perform, I can pay them to go away.

The way the partnership is structured, it’s in their best interest to get the property stabilized and maximize profitability ASAP. It’s in our best interest they succeed, otherwise it will “cost” at least $15,000 to get rid of them.

?Business Plan

The four tenants we inherited from the seller are currently on month to month (MTM) leases. They are currently paying an average of $925 per month. We believe the market rental rate for a 2 bedroom 1 bath unit in Collingswood, NJ is $1,200 per month.

That’s a lot of value to capture.

Here’s how we plan to do it:

- Transition each tenant into our property management system

- Ask all four tenants to sign a 12 month lease at slightly below market rate

- Raising the rents by 20% only gets us to $1,110 per month.

- If they sign, we can delay spending money on updates

- If they leave, we will rehab the unit and put it up for rent at market rate when complete.

- Once all 4 units are leased at market rate, we will refinance the property into long term, fixed rate, amortized debt.

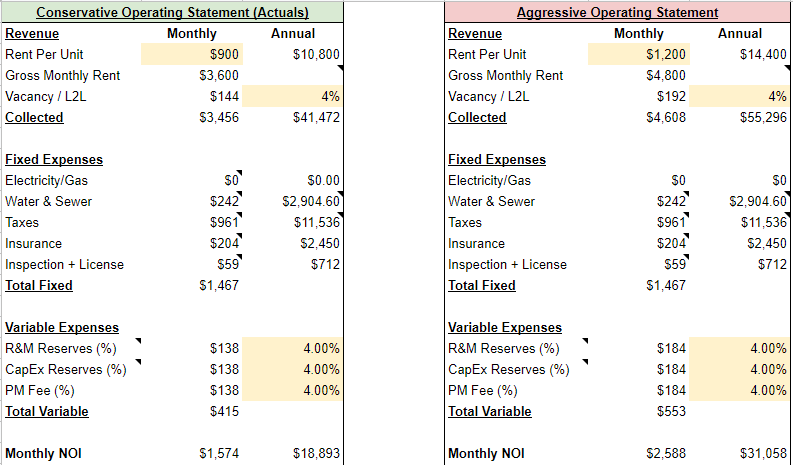

Here is the Actual Operating Statement provided to us by the seller vs. our ProForma.

We can increase the Net Operating Income of this property by $1,000 per month.

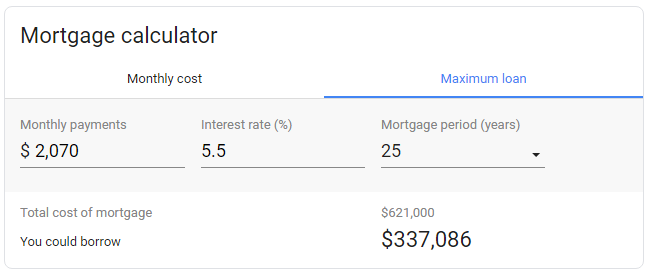

Typically, a lender wants to see a Debt Service Coverage Ratio of 1.25x.

To calculate how much of a loan we can take out, we’d divide our Net Operating Income by 1.25.

$2,588 / 1.25 = $2,070 affordable mortgage payment.

If we assume an interest rate of 5.5% over 25 years, $2,070 will get us a max loan amount of $337,086.

Banks won’t lend more than 70 – 75% of appraised value.

- $337,086 / 70% = $481,551

- $337,086 / 75% = $449,448

Once we’re done with our rehab and have new tenants in place, the property will need to appraise between $450 – $480K.

We estimated the After Repair Value (ARV) to be $450K.

If we can get a new loan for $337,000, my $60,000 will still be stuck in the property. $337,000 + $60,000 = $397,000. We plan on being all in for $400,000. Every dollar saved on rehab is a dollar recovered from my initial capital account.

Let’s see where we land.

?Full Circle

Once stabilized, this property will serve many purposes for us.

- The monthly cash flow will alleviate some of the additional costs of having a kid

- The equity built over time will act as an insurance plan for our kid.

- The equity built over time could also act as a college fund.

- It’s a great way for Dia and I to get back in the driver’s seat of owning our own business.

- It’ll help us build a stronger relationship with our wholesale partners.

- I’m really bullish on these guys. Our first meeting took place in a Chick-Fil-A. Solid dudes.

- The ongoing progress and maintenance of this asset will make for an interesting topic to write about.

SUBSCRIBE NOW TOSUNSHAKSUNDAY

Join my newsletter if you want to learn more about real estate investing, personal finance, health & fitness, and so much more.