I’m in the process of finishing up my first “BRRRR” real estate investment.

I’m referring to the 4-family property we acquired to subsidize the cost of Luna’s education.

If you’re not familiar with the acronym… B.R.R.R.R stands for Buy, Renovate, Rent, Refinance, Repeat.

It’s an advanced method of real estate investing that requires sharp-shooter precision at each stage of the deal.

The end goal of a truly successful BRRRR is to have a cash-flowing asset with none of your own money in the property. It’s more difficult than it sounds.

♻Deal Recap:

Buy: We bought the property on January 24, 2020, for $240,000.

Renovate: We spent an entire year renovating unit by unit as the leases expired for the tenants we inherited. We spent $160,000 (against a budget of $156,000). That’s a win.

Rent: On January 11, 2021, we rented out the last available unit. Our total rent roll increased from ~$3,600 when we bought the property to $5,295 as of Jan 2021.

We’re now ready to refinance and repeat.

?We Used Other People’s Money (OPM)

We raised 100% of purchase and rehab money to fund this deal.

A Private Money Lender funded our down payment ($48,000) and rehab ($160,000).

A Hard Money Lender funded the balance of our purchase ($192,000).

With that said, I’m now looking for a bank to lend $400,000 ($240K + $160K) to pay back my existing lenders.

I need to pay back my existing lenders because the current debt on the property is short-term interest-only financing. That $400,000 was supposed to be paid back within 1 year (January 23, 2021). Seeing as we’re past that date, I need to refinance immediately.

Not only that, we’re paying 8.5% interest on the money.

$400,000 * 8.5% = $34,000 per year or $2,833 per month in interest only! YIKES!

Luckily, we’ve been able to service this debt with the rental income alone. Now that the asset is seasoned and stabilized, it’s time to refinance into long-term fixed-rate debt.

?Refinance:

I anticipated the refinance process would take a few months, so I approached several banks as early as November 2020.

I was so excited because the timing couldn’t be more perfect. Mortgage rates were dropping steadily and every week seemed like a new historical low.

In addition to the historically low rates, we finally found a recently sold comp to value our property against.

The comparable property was updated back in 2017 and sold for $595K. However, it had a detached 4 car garage. It also had one more bathroom (5) but one less bedroom (7).

We have 8 bedrooms, 4 bathrooms, off-street parking, but no garage. With a more recent (2020) renovation, we believe our property is worth $575K.

A $400,000 loan makes for a 70% Loan-To-Value Ratio (400 / 575). A 70% LTV is the maximum a bank is looking to refinance for an investment property. Things are looking up.

?What Goes Up Must Come Down

Towards the end of 2020, everything was going in our favor.

- Renovations were complete.

- We reached full occupancy.

- Rents were high.

- Interest rates were low.

- Property values were high because inventory was low.

All I had to do was find the bank willing to give me the best terms.

I mistakenly thought this would be the easy part.

Why would it be difficult? How could it be difficult? My credit score is 800+. I have ZERO debt. I have the resume. I’m the ideal borrower, right?

I couldn’t be more wrong. Trying to refinance this property has been a humbling learning experience.

Here are the 3 major obstacles I faced trying to refinance this property and how I plan to solve each one.

1️⃣1. Taxable Income Is Too Low

Background:

I’m not shy about minimizing my tax burden. I will do pretty much anything to avoid paying more taxes than I have to.

While this strategy may have marginally benefitted me in the past, it came back to bite me in this instance.

Issue:

Lenders use a formula called “Debt to Income Ratio” to determine whether or not a borrower is likely to be able to pay back a loan.

Lenders like to see a borrower’s debt service to be no higher than ~40% of their taxable income.

I mentioned before that I have no debt. Therefore, the only debt on my balance sheet would be for this property.

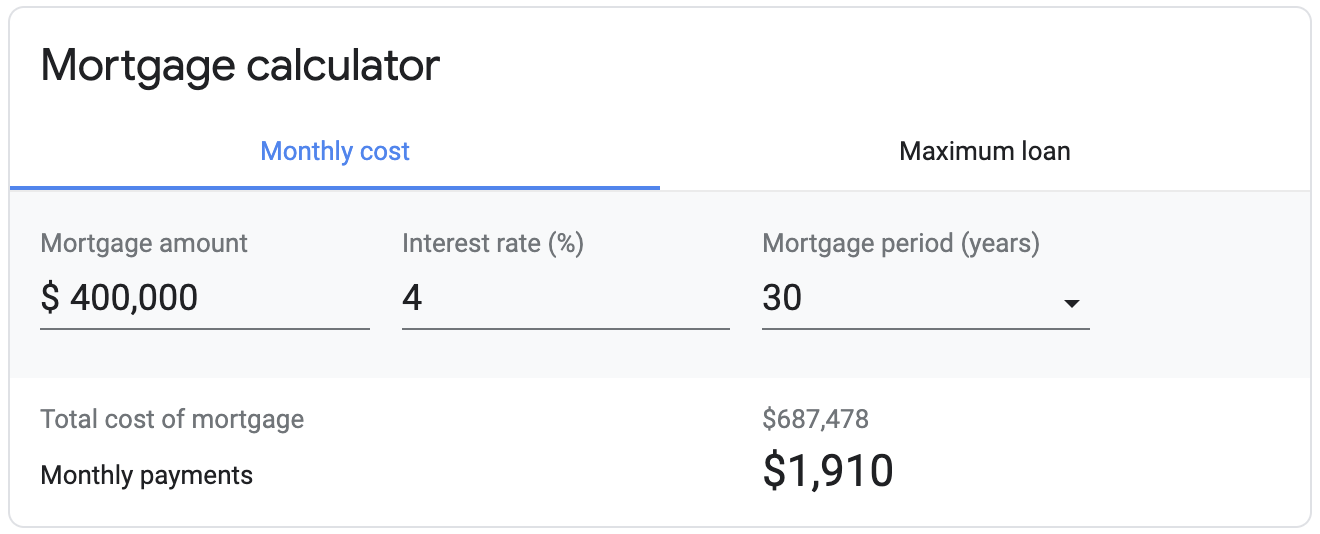

Let’s say I received a loan for $400,000 at 4% over 30 years, the payment would be $1,910 per month for principal and interest alone.

(Rates are generally higher for non-owner-occupied, multi-family homes)

Taxes are $11,500 per year, and Insurance is $2,500 per year. These two items add $1,150 to my monthly payment ($11,500 + $2,500 = $14,000 / 12).

Bringing my total monthly debt service to $3,000.

$3,000 / 40% = $7,500 / month or $90,000 / year required in taxable income.

Here’s where I hit a brick wall.

My taxable income in 2018, 2019, & 2020 is closer to zero than it is to $90,000.

I’ve been so focused on reducing our tax burden that I didn’t anticipate how badly I’d be shooting myself in the foot when it came to refinancing investment property.

Solution:

Once we crossed into 2021, I changed the way I recognize my income for tax purposes.

Instead of paying myself a “Management Fee” as a Contractor (Schedule 1099) for my businesses, I now pay myself as an employee (W-2).

That way, I’m taxed on the gross earnings instead of the net earnings.

Here’s a visual to better explain my point:

I used to be on the right side, but now I’m on the left.

I’m reluctantly giving up the ability to write off expenses against my gross income, but I’m putting myself in a position to be a better borrower in a bank’s eyes.

This won’t pay off until I file our tax return for 2021. The earliest I can expect this adjustment to make a difference is April 16, 2022. Speaking of tax returns…

2️⃣2. My Tax Returns are an Absolute Mess

Background:

I haven’t filed our 2020 Tax Return yet, but it’s “worse” than 2019.

Here’s what my 2019 Tax Return looked like:

- Significant Income through W-2 (Dia)

- Significant Income through 1099-INTEREST (Sunny)

- Significant Income through 1099-MISC (Sunny)

- Significant Losses from 6 different Schedule K-1’s (Sunny)

The total losses from the 6 different K-1’s are greater than our combined income.

Schedule K-1 is the form for businesses that are taxed as a partnership. I’m a general partner in 5 large multifamily buildings, and all of them recognize a loss because of depreciation, which is a non-cash expense.

Trying to explain positive cash flow, but negative returns due to depreciation expense to a traditional bank’s underwriter is like trying to teach Luna how to feed herself. It’s messy.

Issue:

Our joint tax return pulls data from 9(!) different sources of income and losses.

For every non-W-2 data source (of which there is only one), the bank wanted to see the following documents:

- Operating Agreement

- Form SS-4 (EIN)

- Certificate of Formation

- Full Tax Return (not just K-1)

Obtaining this data is a juice that’s not worth the squeeze. I’m a small partner on most of the large multifamily deals. I received 1-2% in Advisor Shares for consulting during the acquisition process.

Bothering my partners with this ask just seems like a total waste of their time. I’m not in the business of wasting other people’s time.

Solution:

Create a holding company in 2021.

I need all of my income sources to roll up into one holding company. That single entity will be the only thing on my tax return, aside from Dia’s W-2 income.

Instead of 9 different data sources, our tax return will only show 2: Dia’s W-2 and my holding company.

I will have the required documents ready for my holding company should a bank ask for them in the future.

3️⃣3. We Don’t Own Our Primary Home

Background:

Dia and I currently rent where we live. I’m still not convinced buying is better than renting.

Issue:

Conventional lending guidelines prevent borrowers from using rental income to qualify for a loan if they do not own their primary home.

I was counting on the rental income to qualify for a loan since my taxable income doesn’t satisfy the debt to income ratio.

Solution:

Since my income alone doesn’t satisfy the debt to income ratio, I have to skip the traditional/conventional lending route altogether.

I’m now looking for commercial loans that require no personal documentation.

?Commercial / No-Doc Loans:

I’m completely removing myself from the equation and letting the asset speak for itself.

A commercial/no-doc loan is typically based on one overarching metric, Debt Service Coverage Ratio (DSCR).

DSCR = Net Operating Income / Debt Service.

Commercial lenders want to see a DSCR of at least 1.25, which means the Net Operating Income is 125% of the Debt Service.

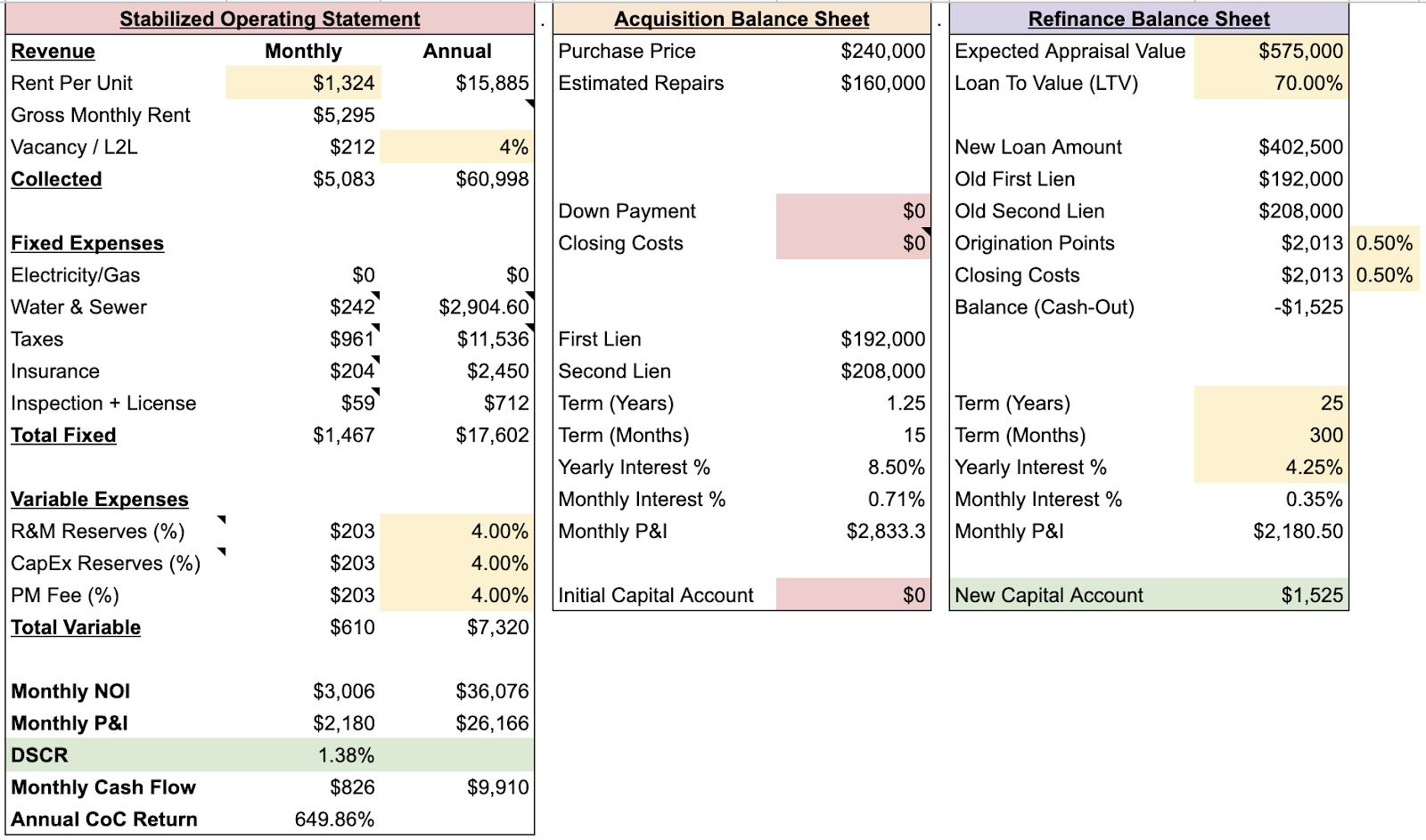

Based on our actual rents ($5,295/month) and expenses ($2,077/month), this property has an NOI of just over $3,000 per month.

Our current commercial lender quoted us the following rate and terms:

- 4.25% fixed for 5 years

- 25-year amortization

- .5% origination fee

- ~$2,000 in closing costs (appraisal, title, etc.)

This computes a monthly principal and interest payment of $2,180.

So the DSCR is $3,000 (NOI) / $2,180 (Debt Service) = 1.38. Bingo!

?Learning Experience

Trying to refinance this investment property has been quite a learning experience.

I thought I had all the qualities of a perfect first-time investor-borrower.

- High credit score

- No debt

- Experience

- Stable property that would pay for itself

Unfortunately, I didn’t check the traditional lender’s boxes.

- My taxable income is too low

- My tax returns are too complicated

- We don’t own our primary home

It’s OK though. Like everything else, this was figureoutable. It took some time, a lot of credit pulls, and multiple introductions to new lenders, but I finally found a solution.

The commercial lender I’m using to refinance this property will lend to me in perpetuity as long as the properties continue to pay for themselves.

Although I’m not ecstatic about having to refinance in 5 years and amortizing the loan over 25 years, I’ll take the win where I can.

On the bright side, a 25-year amortization means a faster payoff, and since this is a no-doc loan the debt will NOT show up on my personal credit history. When we end up buying our primary, the monthly payment for this asset won’t negatively impact our debt to income ratio.

Considering I have a lot of issues to fix by the end of 2021, this is a suitable band-aid for the time being.

SUBSCRIBE NOW TOSUNSHAKSUNDAY

Join my newsletter if you want to learn more about real estate investing, personal finance, health & fitness, and so much more.