On February 9th, 2021, I sold $22,860 worth of the only investment I held in my Roth IRA: FZROX (Fidelity’s Zero-Cost Total Market Index Fund).

Then on February 25, 2021, I contributed $5,000 to my ROTH IRA to max out my annual contribution for 2021. I had previously contributed $500 on January 1st and $500 on February 1st.

By March 1st, 2021 the cash cleared and I had just under $28,000 of dry powder ready to deploy.

Predictable chaos ensued.

Rewind: How I Got Here

Rewind: How I Got Here

Dia and I have both been contributing to our Roth IRAs since she got her first job in the US, which was back in late 2015.

Starting in 2016, we used the tried and true set it and forget it approach. ~$500 automatically transferred from our joint checking account to our respective Roth IRAs on the 1st of every month.

For a while, we were using Wealthfront, a popular Robo-advisor. Then Fidelity introduced their no-cost total stock market index fund: FZROX. The decision to jump ship was a no-brainer.

The max Roth IRA contribution for ‘16, ‘17, & ‘18 was $5,500. The max contribution for ‘19, ‘20, & ‘21 was $6,000

That brings our total contributions to $34,500 over the past 6 years (including ‘21). Today, our balances are a healthy margin higher than that because of how well the stock market has performed.

This brings me to my next point.

Shiny Object Syndrome

Shiny Object Syndrome

Despite the global pandemic and all the hardship that came along with it, 2020 was a fortuitous year for many investors.

The 2020 global stock market crash began on February 20th, 2020, and ended on April 7th, 2020.

If you simply managed to hold your positions, you would have been up on the year. The S&P 500 gained more than 16 percent in 2020. The Dow Jones industrial average and the tech-heavy Nasdaq gained 7.25 percent and 43.6 percent, respectively.

If you had the stomach to buy the dip, your returns would have been even higher. We bought the dip twice. Once on March 1st and again on April 1st. We also periodically bought on the rebound.

Our Rate of Return for Calendar Year 2020 was 20%.

By the time 2021 rolled around, I was feeling a little full of myself. This newly found ego combined with the fear of missing out lead to some foolish decisions.

I wanted in on the crypto-currency, meme stocks, SPACs, and companies wildly benefitting from the “new normal”. Shiny Object Syndrome hit me like a ton of bricks.

Constant vs. Control

Constant vs. Control

Thankfully, I experimented with my account only. Dia’s account stayed the course.

So how did I do with my $28,000?

Let’s see:

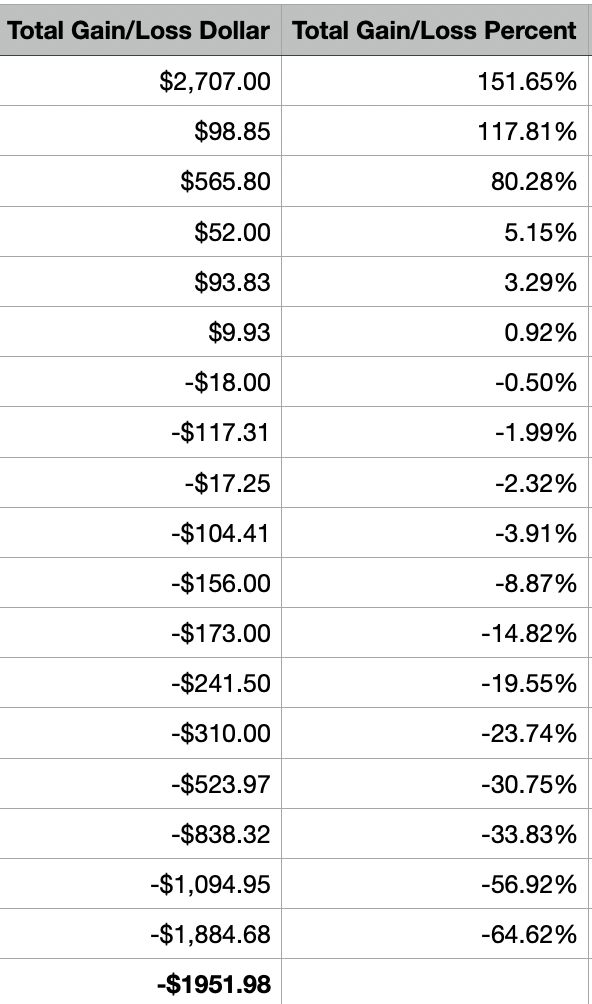

As of July 9th, 2021 I got SMOKED.

I took 18 positions and managed to lose just under $2,000 (as of this writing). Luckily, 3 of those 18 positions had outsized returns that “returned the portfolio”. If those 3 positions were at breakeven, my losses would have been $5,000+.

Now let’s see how Dia’s account did over the same period:

Around the time I started gambling, FZROX was sitting at $13.85 per share. At the time of this writing, it’s at $15.67.

(15.67 / 13.85) – 1 = 13% return.

What was my opportunity cost?

($22,860 + $5,000) * 13% = $3,621. These are the gains I missed out on. Combining this with my actual losses of 1,951 puts me down $5,572.

I am an idiot.

And no, I’m not resulting. I don’t think I’m an idiot because I lost money. I’m an idiot because I strayed from the path I know to be most effective for me as an equities investor.

Lessons Learned

Lessons Learned

Stick to what I’m good at. I’m a decent real estate investor, at best. I’m a TERRIBLE stock picker. I’ve known this about myself. I executed perfectly against this knowledge for years. Why did I stray?

FOMO really got the best of me. I was seeing stocks like Zoom, Peloton, and Amazon predictably crushing it because of COVID and felt like I needed to get in on the action. The action I was seeing on /r/WallStreetBets made me want to get in on the game in a big way.

I’m too emotional. At one point or another, at least 9 of those 18 positions were up 50%+. I was too stupid to take profits off the table because: “![]()

![]() ”.

”.

Trading is stressful. I’m less upset about the $2,000 in actual losses ($5,000+ in opportunity cost) and more upset about the time I wasted being stressed out about the fluctuations in my positions. I checked my accounts more in the past 3 months than I have in the past 3 years.

Moving Forward

Moving Forward

This experience was a good reminder as to why I prefer to set it and forget it by periodically investing in an Index Fund.

One of the most enduring sayings on Wall Street is “Cut your losses short and let your winners run.”

That’s precisely what I’ll be doing here.

First, I’m going to set up stop losses on my biggest winners to lock a modicum of profit. I missed my opportunity to do this earlier, but I won’t let that mistake continue.

Then I’ll put stop loss orders & limit sell orders on my biggest losers. Stop losses protect me from them falling further and limit sells will allow me to recuperate more of my funds.

As these positions are liquidated, I’m going to funnel the money back into FZROX and call it a day.

Once 2022 rolls around, I’ll reschedule my automatic monthly investment and hopefully last longer than 5 years before this happens again.

I’m happy with my ability to recognize the first mistake and avoid the second mistake. The second mistake would be doubling down on my losers or pulling more money out of FZROX to try and make up for my mistakes – effectively throwing good money after bad.

I liken this to going to the ATM at the casino when you lost all the money you came with. You know, the amount of money you were “OK” with losing. Until you actually lose it. At which point you basically negotiate yourself into doing all kinds of stupid things to get it back.

I’ve been prone to doing that in the past. I’m still learning the most important thing to do if you find yourself in a hole is to stop digging.

SUBSCRIBE NOW TO SUNSHAKSUNDAY

Join my newsletter if you want to learn more about real estate investing, personal finance, health & fitness, and so much more.