I’ve spent the last 5+ years self-educating myself on personal finance. I’ve read damn near every book and listened to practically every podcast on the subject.

One of the main things I learned is wealth generation happens in 3 separate phases:

- Make Money

- Keep Money

- Grow Money

More importantly, each phase takes a different set of skills.

I’m an expert at #1. Drop me anywhere in the world with no contacts and I can figure out how to make money by the end of the day. It may not be much, but it’ll be enough.

I’m also pretty damn good at 2. My parents have instilled a saver mentality in me.

Somewhere between 2 and 3 is where my capabilities suffered early on. Every time I saved up a certain amount of money, I’d look for a way to double it in one shot.

I think this behavior stems back to my pre-teen years when my closest friends (to this day) and I became obsessed with gambling.

It started with no-limit Texas Hold’em at the lunch table during the day and in someone’s basement after school and on weekends.

That eventually evolved into visiting Native American Casinos while most of us were still underage.

Then online gambling became a thing. It was easy to deposit money, but good luck trying to withdraw funds from an off-shore bank account.

It was all fun and games when we were gambling away our lunch money. The real trouble started for me once I started making real money in Corporate America.

I kept making the same stupid mistake over and over.

Here’s how it would go: I’d quickly save a bunch of money. Living at home with my parents meant I had no expenses. Ergo, saving $5-10K in a couple of months was routine.

Once I got to “a good number”, I’d place a bet. Maybe it was a stock, a start-up business, or a scheme I came up with to double my money overnight.

The result was almost always the same. I lost it all.

I made my biggest bet in 2014. I had been saving up for years. I had 6-figures tucked away in the bank ready to make my biggest bet yet.

I quit my job, opened a quick-service restaurant franchise, and immediately got my face ripped off. The next 3 years of my life were a living hell.

I promised myself, and more importantly my wife, that I would never make that kind of mistake again.

Not only that, I would dedicate a disproportionate amount of my time learning how to grow our money predictably and securely.

Here’s an attempt to outline our process so you don’t have to learn the hard way by making the same mistakes I did.

💧Liquid

Checking:

The first place our money goes is into our checking account. We use Capital One 360, I’ll explain why later on in this section. Dia’s job, my job, our businesses, monetary gifts from friends and family, etc.

Once we had all our income sources funneling into our checking account, we figured out our monthly burn rate.

Burn Rate = what does it cost to live your life? Rent, groceries, gas, gym, restaurants, entertainment, travel, etc.

If you don’t know your monthly burn rate, this is Homework Assignment #1.

We use Personal Capital to keep track of our spending. You can use another service, like Mint or YouNeedABudget, or do it manually. How you do it is much less important than getting it done.

Saving:

Once our checking account balance equals our monthly burn rate, we funnel money into a savings account. We use Capital One 360 for Savings as well.

Our main Savings account is an Emergency Fund. Our Emergency Fund is anywhere from 3 – 6 months of operating expenses.

We aim to have 6 months of burn, but we will allow it to get down to 3 if we have a lot of unforeseen expenses. Then we commit to building it back up over time.

This emergency fund came in handy when COVID-19 hit and Dia was on extended maternity leave.

Sub-Savings:

This feature is the single biggest reason I recommend using Capital One 360.

After your Emergency Fund is fulfilled, you can open multiple “Sub-Savings” accounts for large purchases in the distant future.

Sub-Savings accounts make those inevitable large purchases much more digestible.

Here are a few examples of our sub-savings accounts:

Charitable Contributions: We send a fixed amount to this account every week. At the end of the year, we make a one-time lump sum donation to our preferred non-profit organization (INADCure.org). Dia’s company will typically match our gift so our contribution goes twice as far.

Travel: We send a fixed amount to this account every week. Whenever we travel, we use our Chase Sapphire Reserve card to book flights, hotels, and tours and then immediately pay off those expenses from this account.

House Down Payment: I regret not starting this earlier. If we had started this sub-savings account back when we started the others, we would have 4 years of money piled up and ready to deploy.

None of this is Rocket Science. In fact, it’s pretty simple and boring. The unsexy truth about money is boring is better.

🔢 Tax-Advantaged Retirement Accounts

Now that we have the immediate future taken care of, let’s shift our focus to long term investments.

Employer-Sponsored Retirement Plans – 401(k) or TSP:

The first investment we make is towards Dia’s 401(k).

We personally select the Traditional option instead of ROTH because we’re looking to minimize our tax bill today, not in the future.

Another benefit of employer-sponsored retirement plans is there might be a match up to a certain amount of your contribution.

If your employer matches a portion of your 401(k) / TSP contribution, you should be contributing AT LEAST that amount every single year.

Dia’s company matches contributions up to 4.5% of her paycheck.

As a self-employed individual, I don’t have this option. I contribute to something called a SEP IRA. It’s like a 401(k) for self-employed people.

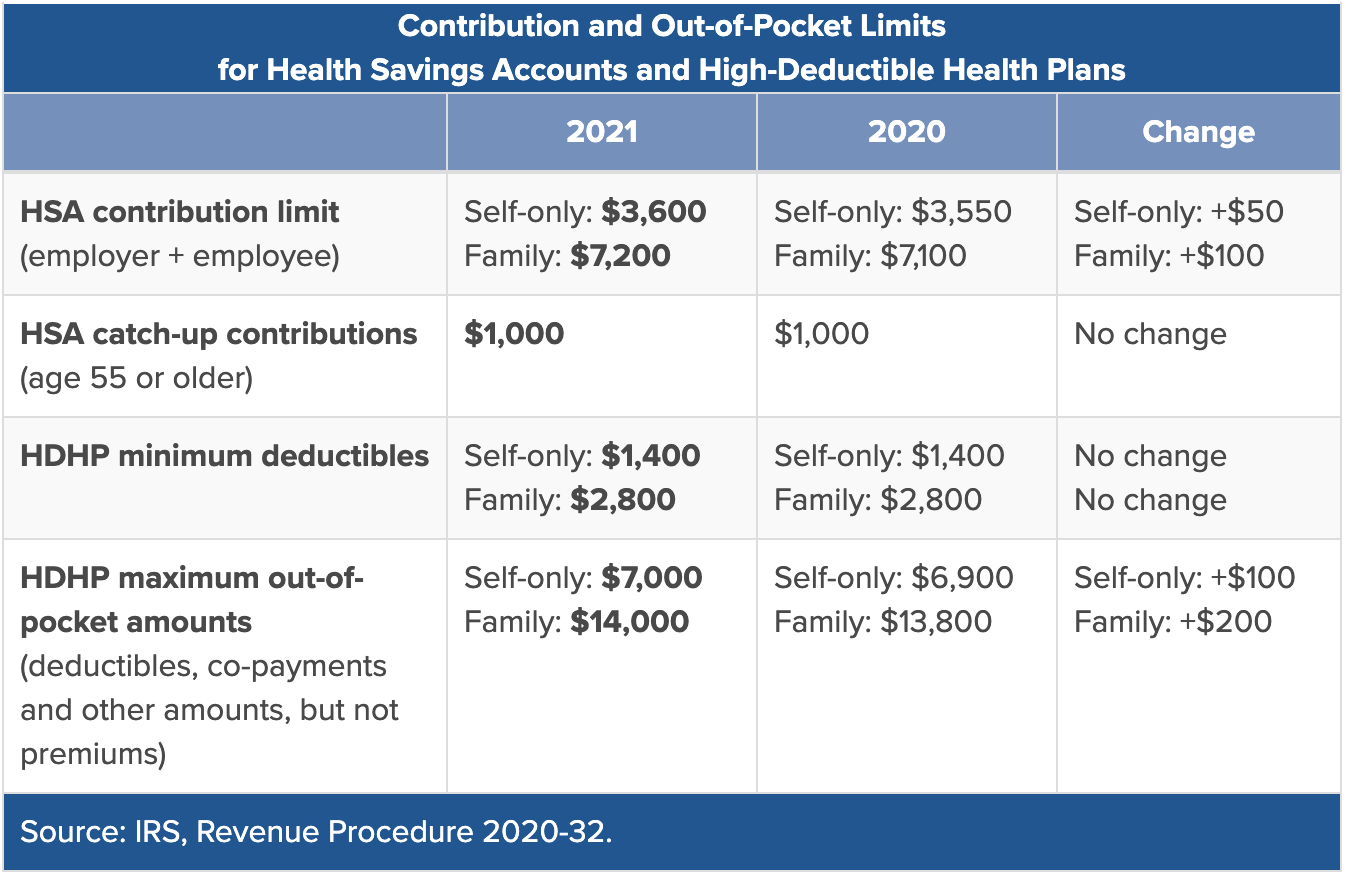

Health Savings Account:

Once we met Dia’s employer’s contribution match amount, we began contributing to a Health Savings Account. We use Fidelity.

Disclaimer: to be able to contribute to an HSA, you need a High Deductible Health Insurance Plan.

Please see the chart below to see contribution limits, minimum deductibles required, and maximum out of pocket amounts:

The HSA is a great tool because it’s triple tax-advantaged:

- The money you contribute is tax-deferred

- The money then grows tax-free if invested

- If the principal & growth are spent on Health Care related costs it’s also tax-free

IRA:

After you max out your HSA, you could look into opening an IRA. If you have an employee-sponsored retirement plan, you cannot take advantage of a Traditional (tax-deferred) IRA.

So you open a ROTH IRA instead, which uses post-tax money for contributions. The benefit of a ROTH IRA is the growth is tax-free. We use Fidelity for this also.

There are some nuances for ROTH IRA contribution limits. However, you should be able to contribute $6,000 per year if you’re less than 50 years old, and $7,000 per year if you’re more than 50 years old.

The reason we use Fidelity for both our HSA and IRA is Dia’s employer-sponsored 401(k) is through Fidelity. It’s just easier to keep everything in the same place.

FWIW: If we weren’t anchored into Fidelity, I’d prefer to use Vanguard.

Back to your Employer-Sponsored Retirement Plan:

Once you’ve met the following criteria…

- Contributed up to employer match

- Maxed out HSA

- Maxed out IRA

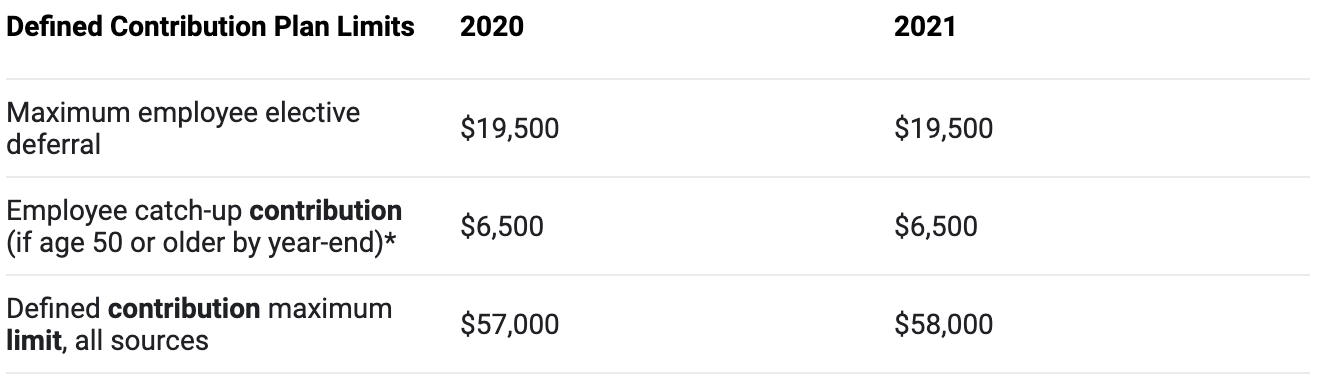

… you can go back to your employer-sponsored retirement plan and contribute the max there as well. The max is $19,500 if you’re less than 50 years old and $26,000 if you’re more than 50 years old.

The $58,000 number is for companies with profit-sharing plans. These are rare so I won’t be covering them here.

♻Intermission:

We’ve covered the basics. Let’s recap where we are so far:

We have 1 month of operating expenses in our checking account. Your balance hardly changes on a month to month basis. As new money comes in from wages, salary, or investment income, old money goes out to pay off your lifestyle: rent, gas, utilities, groceries, restaurants, clothes, etc.

We have 6 months of operating expenses in a savings account. You use this account for emergencies only. Anything from replacing a blown-out tire to funding a month or two of living while you’re in-between jobs. Anytime money comes out of this account, it should be replenished steadily.

We have sub-savings accounts set up with automatic transfers to help ease the pain of larger long term expenses and investments. You can get as granular as you want. You can save up $1,200 over 36 months for a new set of tires. Or you can keep it big picture and save for the handful of things everyone complains about spending money on at one point in their life (wedding, down payment, car).

We maxed out all of our tax-advantaged retirement accounts, which means you’re contributing just over $29,000 per year in tax-deferred investments between your HSA ($3,600), your IRA ($6,000), and your 401(k) ($19,500).

Everything up until this point is pretty straight-forward and agreed upon by the online personal finance community. However, there’s less consensus on what to do next.

Here’s what I’ve found to work best so far.

📜Term Life Insurance:

If you’re reading this post and are still interested, I’d venture to guess you’re a planner like me.

There are some things in life, however, that you just can’t plan for. Death is the primary example.

None of us know when we’re going to go. The best we can do is prepare as if today’s our last day. RIP Kobe & GiGi![]() .

.

What would it mean, from a purely financial perspective, if you were to die today? Is your family secure without you?

In my relationship, if we lose one person’s income, it would mean the surviving partner would have to make a HUGE lifestyle change immediately.

Term Life Insurance is an inexpensive way to alleviate the financial stress of an income-producing family member’s passing.

How much is enough?

A Financial Planner may suggest 10x your gross annual income. I don’t know if there’s a perfect formula out there, but here’s how I think about it.

3 years of combined gross income. If I pass away tomorrow, the last thing I want Dia to have to do is go back to work before she’s ready because she “has” to. Kill me again for having failed my wife.

Debt Balance. If you have a joint credit card, student loan debt with a spouse or parent as a guarantor, or a mortgage co-signed by a spouse or parent, please consider adding these debt balances to your life insurance policy.

Don’t leave your loved ones holding the bag of your YOLO tendencies without having the benefit of being with future you.

Add up all your debt, multiply it by 1.25 and add it to your Life Insurance tab. Actively work towards paying off all your debt and avoid encumbering yourself further.

$500K per child. The USDA calculates it costs $233,610 to raise a child from 0-18 years old. So half of that $500K is just to get them to 18. In most cases, that’s enough.

But if you’re like me and had your advanced education paid for by your parents, you likely want to pay it forward. That’s where the other $250K comes in.

I guess I do have a formula. It’s:

- 3 years of combined gross income

- Total Debt Balance: credit, personal, student, auto, mortgage, HELOC

- $500K per child

If you don’t know where to start when it comes to Term Life Insurance, I suggest using PolicyGenius to get a quote. I think you’ll be surprised by how inexpensive it is.

Their 4 step process is as easy as ordering a burrito bowl at Chipotle.

A 25 year $1,000,000 policy for me costs just under $50/mo. That’s $15,000 spent over 25 years. If I don’t end up dying, I’m pretty sure I won’t be too sad about it.

If I do end up dying, it’ll be the best $50/mo I spent while I was alive. After the $50/month we spend on Netflix, Hulu, Disney+, HBO Max & Spotify of course.

🏠 Investment Property

Once you take care of your personal future through tax-advantaged retirement accounts and your family’s future through term life insurance, you can refocus on the present.

Cue the mailbox money. Everyone should strive to have passive income that doesn’t rely on their time or effort the way a job does.

Rental Real Estate is the best way I know how to generate reliable passive income. It may take a lot of work up front, but once your systems are in place, the $/hr rate is virtually limitless.

💥 Risky Business

We finally reached the tip of the pyramid. I call this portion of our investment strategy “risky business”.

This is where we allocate less than 5% of our net worth to “10-baggers”. Strategically placed bets that can potentially yield a 10x return on our initial investment.

These are the ideas you pick up from /r/wallstreetbets.

Or maybe you know someone starting a consumer packaged goods company and they’re raising a friends and family round.

Or maybe you follow a SPAC sponsor that makes all of his investments public through his Twitter account and you ride his wave.

Or maybe you take a flier on the latest cryptocurrency.

Warning: be prepared to lose this money. If something has the potential to yield a 10x return, it’s just as likely to go to zero.

If you don’t have everything we talked about above in place, please DO NOT expose yourself to risky business. These types of investments were the bane of my existence when I got my first job. This is where I went first when I should have been saving it for last.

🧠TL;DR:

If you want to grow your wealth systematically, take the boring and systematic approach. Automation is your friend. Set up recurring transfers and automatic investments. Let the system do the work.

Treat yourself like a business. If there’s no money left over at the end of the day, focus on increasing your income and optimizing your expenses. Get familiar with your monthly burn rate. Create an emergency fund equal to 6 months of operating expenses.

Taxes are the silent killer and probably your biggest expense line item. Play offense. Reduce your tax bill today by maxing out all of your tax-advantaged retirement accounts.

Memento Mori: You could leave life right now. Let that determine what you do, say, and think. Protect your family financially with term life insurance.

Create passive streams of income that don’t rely on your undivided attention, time, and effort. Rental Real Estate is a great source of mailbox money. It also has tax advantages and scales well.

Once you have all your ducks in a row, create a fun fund. Allocate less than 5% of your net worth to moon shots .

.

SUBSCRIBE NOW TOSUNSHAKSUNDAY

Join my newsletter if you want to learn more about real estate investing, personal finance, health & fitness, and so much more.