In September of 2019, the United States Bureau of Labor Statistics published a Consumer Expenditures report for the years ending 2016, 2017, & 2018.

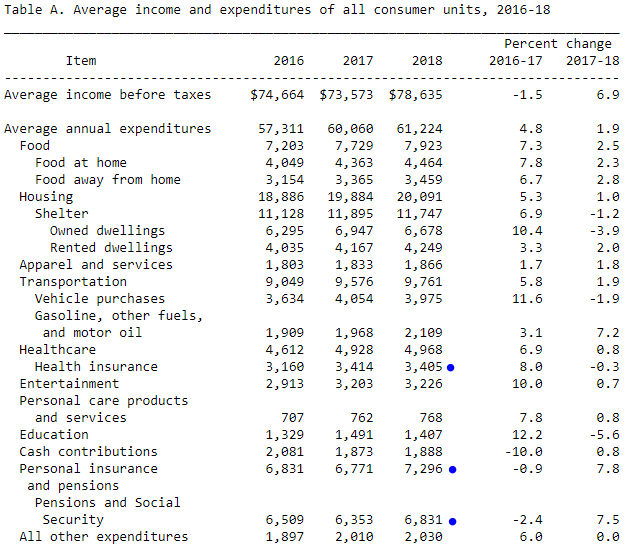

See Table A. Below.

The average income before taxes per consumer unit for 2018 was $78,635.

The average expenditure per consumer unit for 2018 was $61,224.

Source: BLS.gov

*The meaning of the blue dots will reveal themselves later.

Table A. does a great job outlining how much the average consumer spends in each category. However, there is a major expense missing. Can you guess what it is?

Here’s a hint: “Only 2 things in life are guaranteed…”

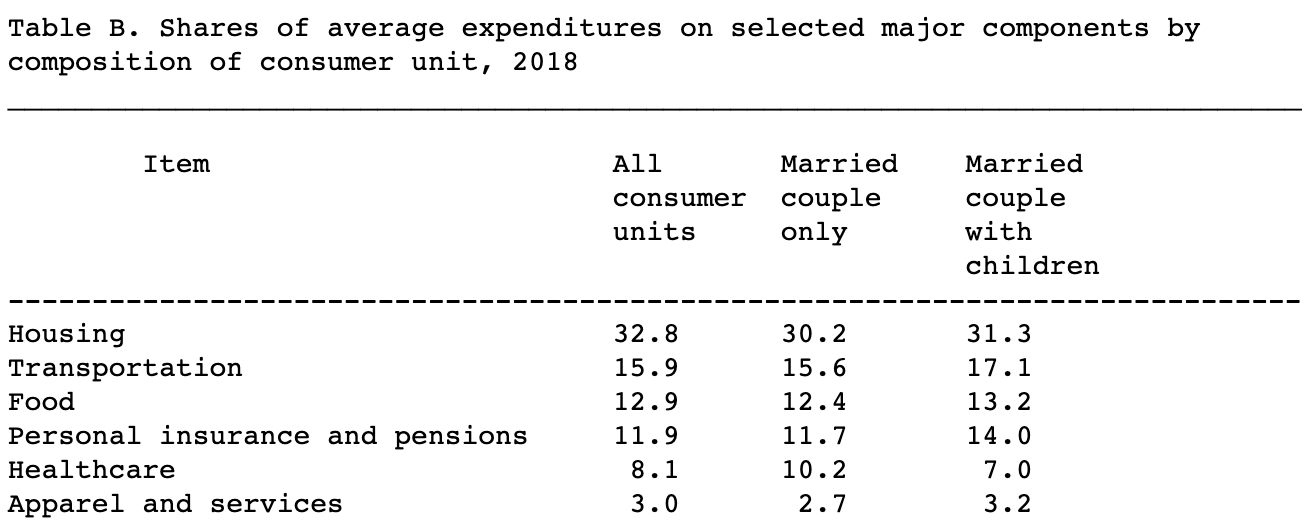

Before I address the missing expense, let’s look at the major components of expenditure by composition of the consumer unit. See Table B. below.

Source: BLS.gov

In each scenario, roughly 60% of total consumer expenditure went to Housing (30%), Transportation (16%), & Food (13%).

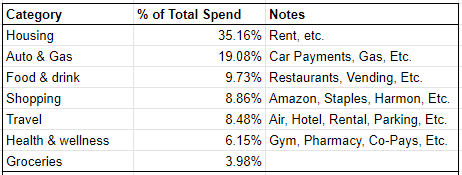

As I was writing this article, Chase Bank published their year end review statements for 2019. Naturally, I made the chart below.

Chart Notes:

- The % next to each category is calculated off total spend.

- I removed our IVF spend from the equation as it is an outlier.

- I manually added Rent & Car Payments as those expenses are paid through debit, not credit. No other debit expenses are included.

It looks like we’re in line with the average American consumer! Our top 3 expenses are the same: Housing, Transportation, & Food.

It's worth mentioning my model is imperfect. Dia and I routinely pay the total bill when dining at restaurants or traveling (airfare & hotel) with friends. They reimburse us for their share through Venmo. The reimbursed dollars are not reflected in the chart above.

This is me hedging. I don’t want to be judged for spending 2.5x on Restaurants over Groceries.

Back to The Missing Expense: Taxes.

Here’s what I don’t understand. Why didn’t the United State Bureau of Labor Statistics include Taxes? It is an expense every American consumer unit pays.

Here’s my best guess: If they included income taxes, the delta between stated income and expenses would evaporate.

Taken straight from Table A.

$78.6K: 2018 Average Consumer Unit Income

$61.2K: 2018 Average Consumer Unit Expense

$17.4K: 2018 Delta

$17.4K: Are we to assume this is what the average American saved in 2018?

Nope. Because... taxes.

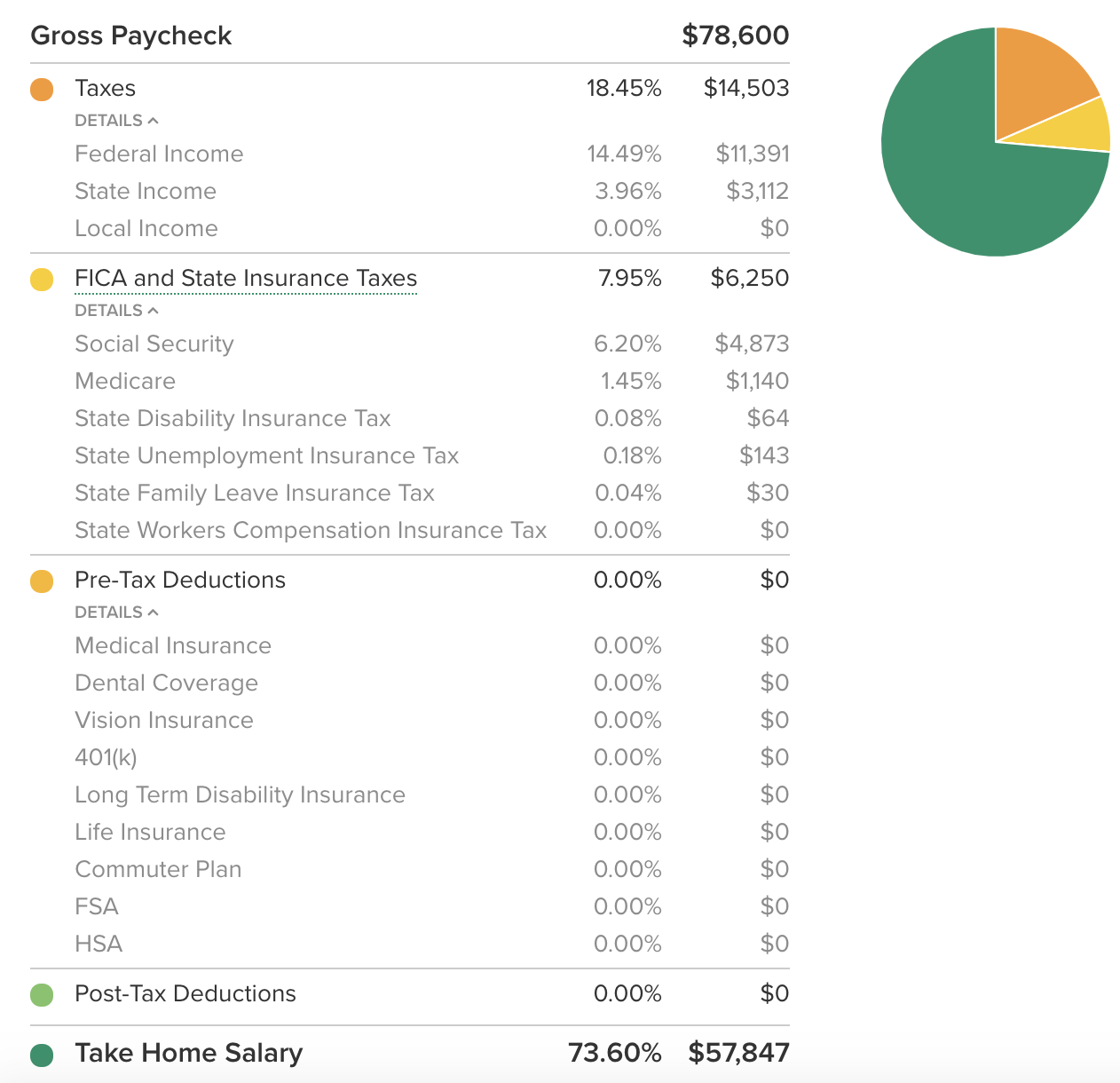

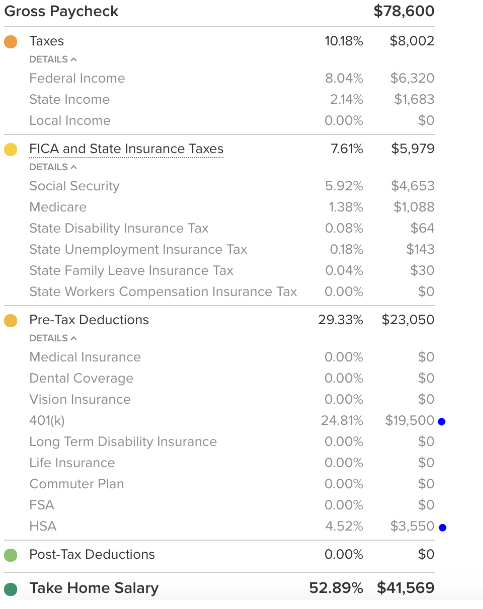

Let’s run the numbers. Here’s what the Income Tax looks like for a Single Tax Filer making $78,600 per year in New Jersey. Double check my work: You can run the numbers yourself on smartasset.com

Source: Smartasset.com

Based on this chart, the after tax take home pay for the average American Consumer Unit (in NJ) is $57,847. That’s $20,753 spent on taxes. =(78,600 - 57,847)

How is it possible for someone to take home $57,847, but spend $61,224? What am I missing?

Well, a few things.

First, we have to adjust the Income Tax chart with the expense line items that qualify as “Pre-Tax Deductions” in the USDL’s Table A.

We do this because Pre-Tax deductions reduce the taxable income. So if someone makes $78,600 per year, but has $5,798 in pre-tax deductions, their taxable income becomes $72,802. =(78,600-5,798). Less taxable income = less taxes payable.

Here are the Pre-Tax Deductions in the USDL chart (marked with blue dots in Table A above):

- $3,405: Health Insurance

- $465: Personal Insurance =(7,296 - 6,831)

- $1,958: Pension (Social Security is $4,633 of $6,831)

Here’s the updated Income Tax chart with Pre-Tax Deductions:

Source: Smartasset.com

The new take home pay went down, but so did our tax burden. Without accounting for the pre-tax deductions, taxes payable used to be $20,753. They are now $18,795. =(12,841+5,954)

Now, we know the tax burden for the single filer making $78,600 in New Jersey: it’s $18,795.

Bringing their total take home pay to $53,976.

We’re not done yet.

Now we have to adjust the annual spend from the USDL report to take out the costs we’re counting twice.

$61,224 (Total Spend in 2018)

- 4,633: Social Security

- 3,405: Health Insurance

- 1,958: Pension

- 465: Personal Insurance

The new total spend per average American Consumer Unit? $50,763!

=(61,224 - 4,633 - 3,405 - 1,958 - 465)

Here’s Our New Delta:

$53,976: 2018 Take Average American Consumer Unit Home Pay

$50,763: 2018 Average American Consumer Unit Expenditure

$3,213: 2018 Delta

Phew! Americans are in the black by the skin on their teeth.

Credit Cards

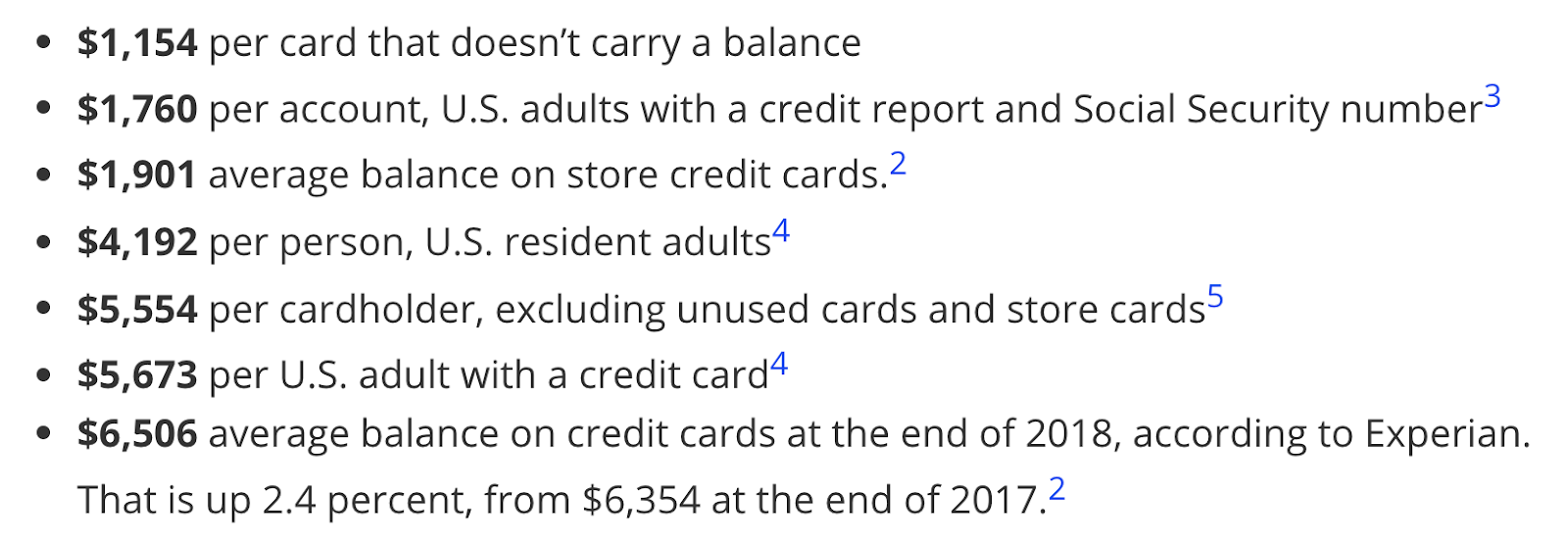

Something still doesn’t add up. If there’s a net positive delta of $3,213 between average income and expense, why does the average American have credit card debt?

According to this Research & Statistics article on creditcards.com, the average consumer credit card balance is between $1,760 and $6,506.

Source: Creditcards.com

Question: Is the average American consumer unit “saving” $3,213 then knowingly carrying a balance on their credit cards?

No way. That’s irrational behavior.

The interest alone over one year on a $6,500 credit card balance can be upwards of $1,500. That’s 50% of what was “saved”.

What Am I Getting At?

My apologies, I got carried away with the math and charts.

I’m trying to make two points:

- Taxes are a much higher expense (as a % of income) than people think. But there’s something we can do about it with pre-tax deductions

- Take a page out of Warren Buffet’s book: “Do not save what is left after spending; instead spend what is left after saving.”

It’s possible to kill two birds with one stone here. Save more money while reducing your taxable income.

Contribute to Tax Advantaged Retirement Accounts:

- 401k & 403b

If you work at a large company, you may have access to a 401(k) plan. Sometimes this is also called a 403(b). The basic difference is that a 403(b) is used by nonprofit companies, religious groups, school districts, and governmental organizations.

For 2020, they both have a contribution limit of $19,500. If you’re 50 years or older, you can contribute an additional $6,500 as a “catch up contribution”.

The plus side to the 401k contributions is that it reduces your taxable income, which in turn reduces your tax liability. The down side is it’s cost prohibitive to touch the money until you reach retirement age, which is 59.5 years old.

Isn’t it better to keep your hard earned money and wait for it, rather than pay more taxes? Taxes paid are dollars you’ll never see again.

Finally, since you don’t pay any taxes on the 401(k) contribution dollars when they go in, you have to pay taxes on the money when it comes out.

There are two schools of thought here:

- Taxes seem to always be rising. Better to pay taxes today instead of tomorrow

- Defer taxes today, invest more, the additional gains will outweigh the tax increase

I believe a bird in hand is worth two in the bush. I can realize a gain now (pay less income taxes), and maybe again later if the rules change.

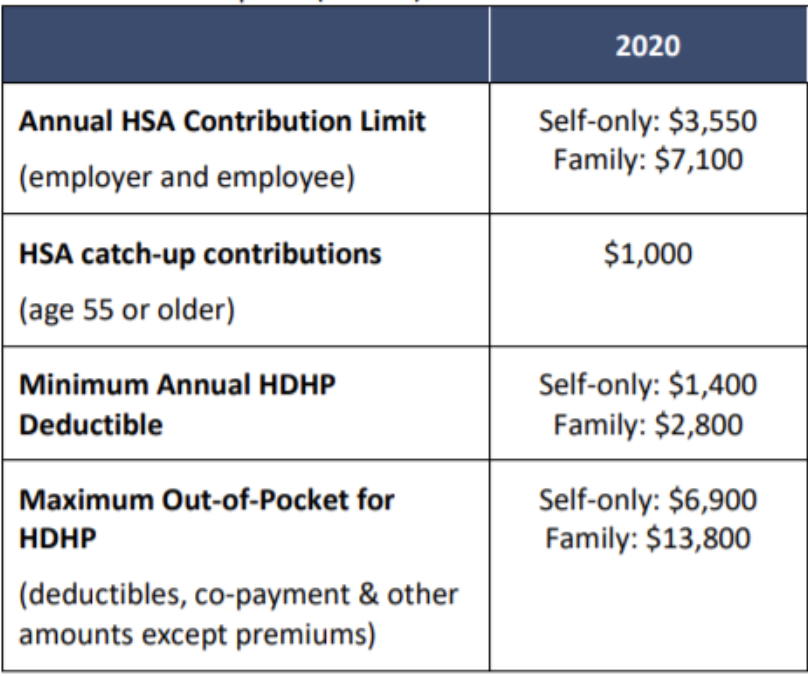

- HSA (Health Savings Plan)

If you have a high deductible health care plan, you can contribute to something called an HSA.

Check your health insurance card. Is your deductible higher than $1,400 for an individual or $2,800 for a family? If yes, you can contribute to a HSA plan.

For 2020, the maximum you can contribute to an HSA is $3,550 as a single filer, or $7,100 as a family. If you’re 55 years or older, you can contribute an additional $1,000 as a “catch up contribution”.

Source: BenefitAdvisorsNetwork

HSA’s are often referred to as the Ultimate Retirement Account because they are triple tax advantaged.

- You don’t pay taxes on the money going in.

- If the funds are invested, you won’t pay taxes on any gains realized.

- You won’t pay taxes on any money taken out as long as it goes towards a health related expense.

Once you reach 65 years old, you can pull money from your HSA like any other tax deferred retirement account. The money doesn’t need to be used on health related expenses.

Dia’s company offers a high deductible and low deductible health insurance plan. We chose the high deductible plan because 1) We’re young and healthy and 2) We want to contribute to a Health Savings Account.

BTW: We paid for IVF with the money from our Health Savings Account. That made a HUGE difference for us considering how much that procedure costs.

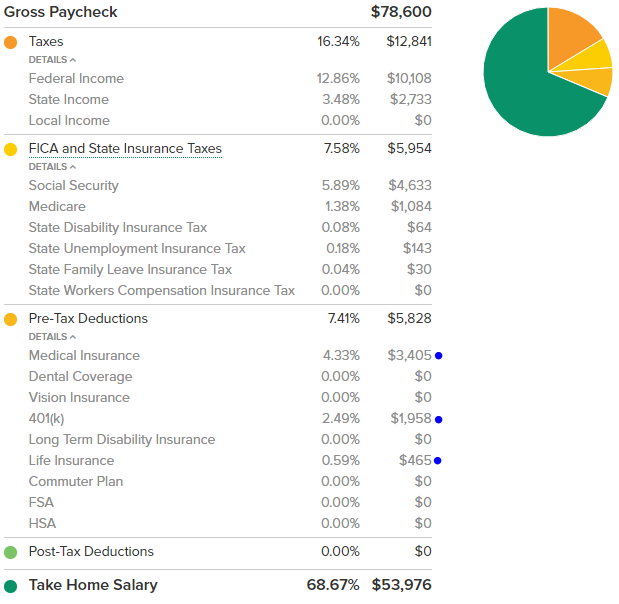

Let’s pause here. I want to show you the benefit of contributing the max to these two accounts (401(k) & HSA).

Source: Smartasset.com

So I plugged in $19,500 for the 401(k) and $3,550 for the HSA (new blue dots) into the income tax calculator. These are both Pre-Tax Deductions, which means they reduce taxable income. I used the same income as the average American consumer unit: $78,600.

Before, without these two investments, our income tax payable on an income of $78,600 was $20,753.

- $14,503 - Federal, State, & Local Taxes

- $6,250 - SS, Medicare, Disability, Unemployment, etc.

Now, you can see the tax liability totals $13,981.

- $8,002 - Federal State & Local Taxes

- $5,979 - SS, Medicare, Disability, Unemployment, etc.

We just killed two birds with one stone:

- We invested a total of $23,050. =(19,500 + 3,550)

- We reduced taxes payable by $6,772. =(20,753 - 13,981)

However, we can’t just gloss over the fact that our take home pay went down to $41,569. That’s $16,278 less than the $57,847 we had before making these tax deferred investments. =(57,847 - 41,569)

That’s much less purchasing power for the average American consumer unit. Almost $1,400 per month less. =(16,200 / 12)

Birdseye View: What’s the immediate net gain here?

- + 23,050: 401(k) + HSA (money kept, but can’t use until retirement age)

- + 6,722: Tax Savings (money not paid to Uncle Sam)

- - 16,278: Reduction to Take Home Pay

- = 13,494.

Although take home pay reduces, net worth ultimately increases by $13,494.

I especially like the 401(k) and HSA because they are typically automatically deducted from the paycheck and routed to their respective custodians. (i.e. Fidelity, Vanguard, etc.)

This automation removes discipline and will power from the equation. Out of sight out of mind.

No 401k? No Problem

There are other tax advantaged retirement accounts you can take advantage of. The following accounts typically require an extra step. You have to send money from your bank account to the custodians. It’s much more difficult to save & invest this way.

For these retirement accounts, I recommend setting up a recurring automatic transfer the same day your paycheck hits your bank account.

- SEP IRA

SEP stands for Simplified Employee Pension. These tax deferred retirement accounts are typically used by Self Employed people. If you recognize your income as a 1099 Contractor instead of a W2 employee, you’re eligible to contribute to a SEP IRA.

SEP IRAs were primarily designed to encourage retirement benefits among businesses that would otherwise not set up employer-sponsored plans. Sole proprietors, partnerships, and corporations can establish SEPs.

The contribution limit for the SEP IRA is high. In 2020, you can contribute 25% of your taxable income, up to $57,000. To max out the contribution of a SEP IRA, your taxable income must be $228,000. =(57,000 / 25%)

- Traditional IRA

The traditional IRA is the same as the SEP IRA and 401K except it has a lower contribution limit. For 2020, your total contributions to your traditional IRA cannot be more than: $6,000. If you’re 50 years or older, you can contribute an additional $1,000 as a “catch up contribution”.

Talk To Your Accountant

Here’s the magic question: What can I do to pay less taxes today?

I mentioned the contribution limits for each account.

- 401(k): $19,500 (+ $6,500 catch-up)

- HSA: $3,550 individual / $7,100 Family (+$1,000 catch-up)

- SEP IRA: Lessor of $57,000 or 25% of Income

- Traditional IRA: $6,000 (+1,000 catch-up)

However, there are also income limits to consider. Meaning, you may get phased out of using certain accounts if your income is too high.

For example, in 2020 you cannot contribute to a ROTH IRA if you make more than $124,000 as a single filer. If you are married and filing jointly, you cannot contribute to a ROTH IRA if your combined income exceeds $196,000.

I didn’t go into detail on ROTH IRA’s in the list above because those contributions are made with after tax dollars. The ROTH is still a great tax advantaged investment vehicle. I just recommend prioritizing the tax deferred accounts first.

Hedonic Adaptation

Giving up purchasing power today in order to secure a better future is a difficult task to fulfill.

Delayed gratification is not something we’re used to practicing in the current state of the “demand economy”.

In this particular scenario, I suggest the average American consumer unit reduce their take home pay by 16K per year so they can pay less taxes (6K), and have access to savings in retirement (23K).

It would be a less demanding proposition if each consumer unit operated on a delta of more than $3K per year. However, we are where we are.

Let’s not forget…

When push comes to shove, people are really good at adapting to new environments and situations. We have a tendency to normalize exciting new opportunities just as quickly as we can normalize unfavorable conditions.

I drove my dinged and dented Rav4 for 10 years and 150,000+ miles. Then I found myself in a fortunate position to acquire a Tesla Model 3. For months, I smiled ear to ear every time I got in the car. Today, I’m still grateful, but the car has admittedly reduced to my new normal.

People often view hedonic adaptation through the lense of lifestyle enhancement. It also works the other way.

I used to work at one of the top consulting firms in the country. Compensation was great, work life balance was amazing, and the people were top notch. I quit that cushy gig to go into business for myself. For three years I made no money, worked 80 hours per week, and had nothing to show for it. A month or two into that endeavor, those conditions became my new normal.

It may seem impossible for the average American consumer unit to give up $1,400 per month in take home pay, but I fully believe they can adapt.

I’m trying to reinforce the words of Warren Buffet:

- “Do not save what is left after spending; instead spend what is left after saving.”

Reduce take home pay today by investing in tax deferred retirement accounts. It’s going to suck to have less pocket money, but you will adapt. It’s what we do. Switch your focus to spending less or earning more. Either works. I suggest earning more.

Your future self will thank you.

- “Someone’s sitting in the shade today because someone planted a tree a long time ago.”

Be that someone for yourself.

Did someone forward you this email? Click Here to join SunShakSunday.